Dynamic Risk Management Using Rolling Stock Price Metrics

Equation. 1: Formula illustrating the computation of daily historical volatility. The calculation is based on returns of stock prices and provides a measure of how much the stock has fluctuated on a day-to-day basis in the past.

Equation. 2: Formula for converting daily historical volatility to annualized volatility. The transformation incorporates the square root of the number of trading days in a year (typically 252), offering a more long-term perspective on stock price fluctuations.

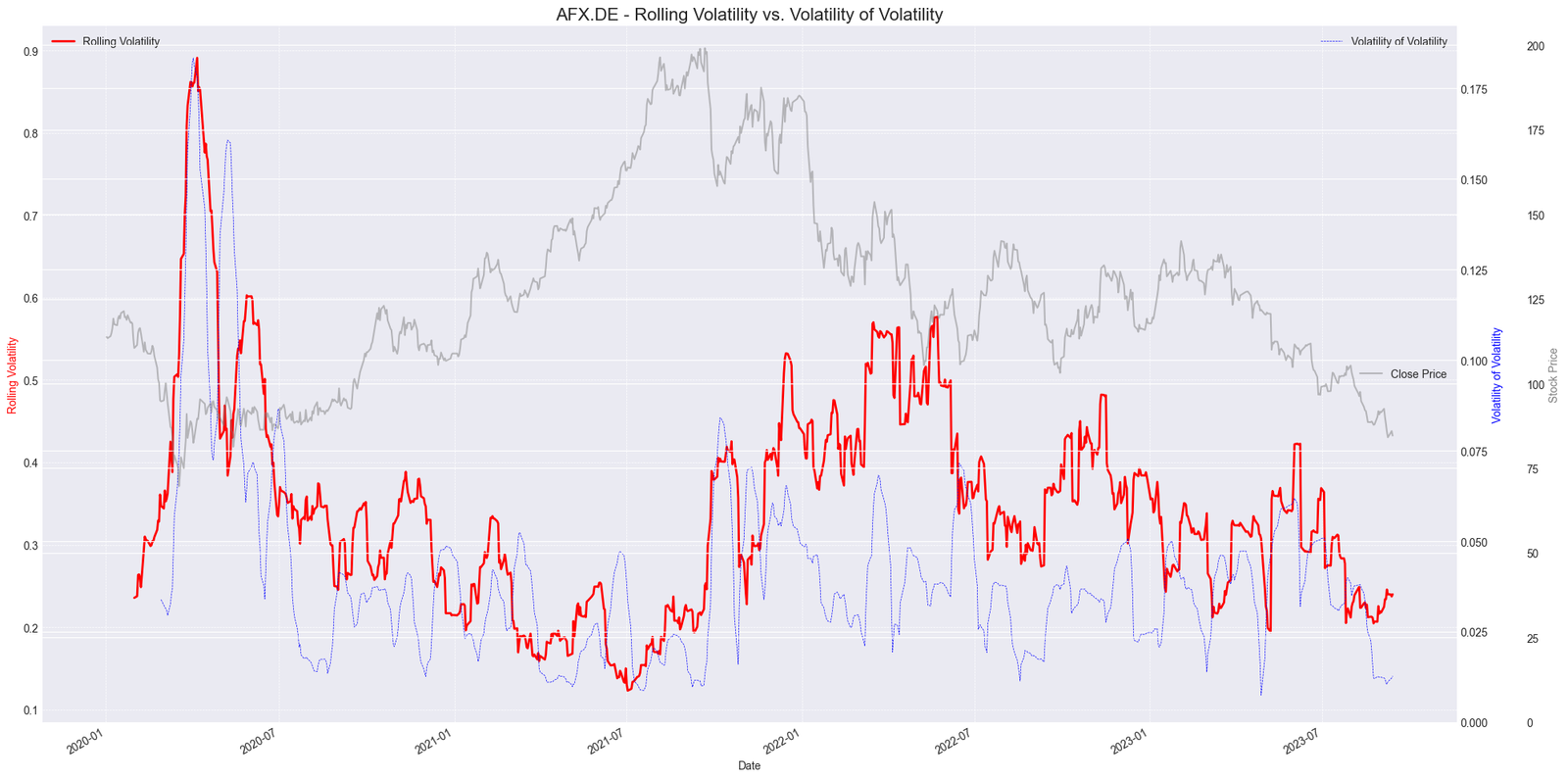

Figure. 1: The graph presents a multi-dimensional view of “AFX.DE” stock dynamics over time. The red solid line depicts the 21-day Rolling Volatility, highlighting periods of significant price fluctuations. In blue dashed lines, the Volatility of Volatility (VoV) offers a meta-view of the stability of the rolling volatility itself. The translucent grey line traces the stock’s closing price throughout the period. Together, these metrics provide a comprehensive insight into the stock’s risk profile and price evolution.

Equation. 3: Formula for the Sharpe Ratio, which measures the performance of an investment relative to the risk-free rate, adjusted for its risk.

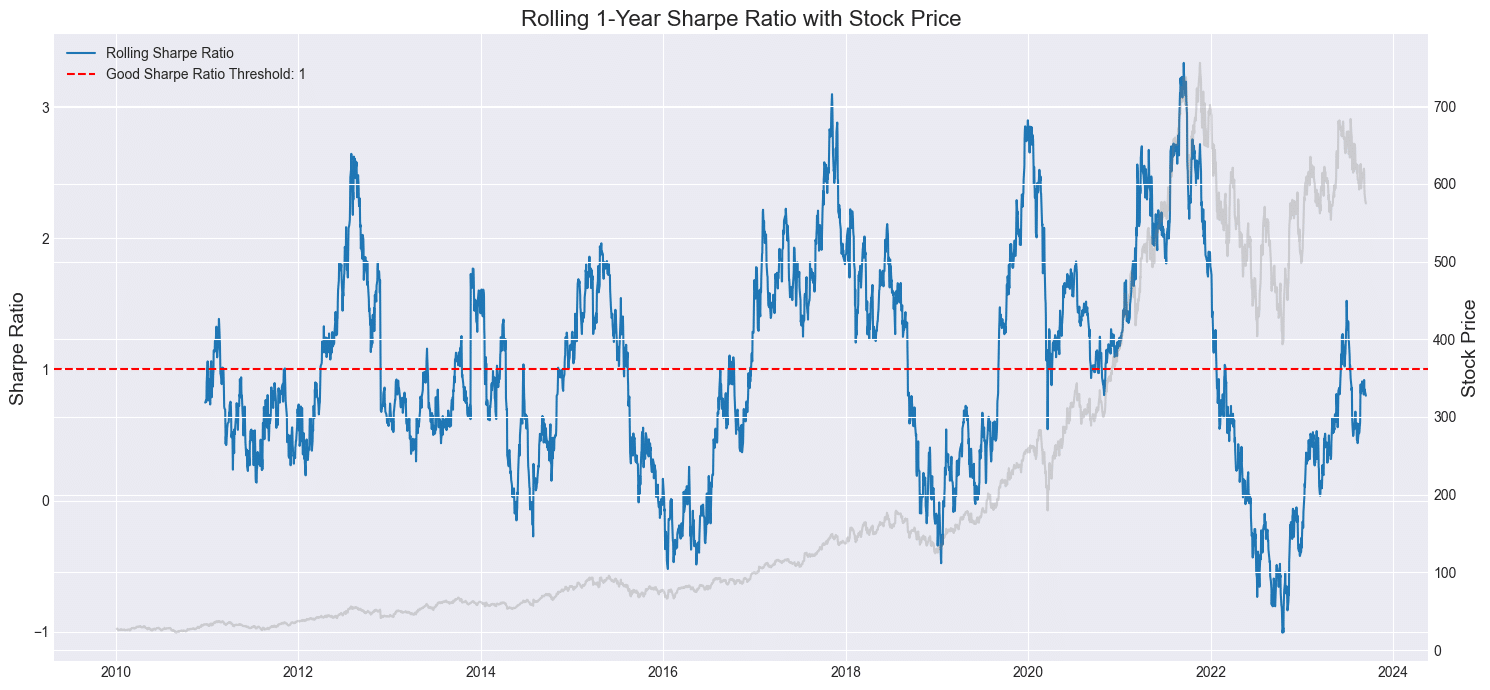

Figure. 2: Visualizing the 1-Year Rolling Sharpe Ratio for “ASML.AS”: Balancing Risk-Adjusted Returns against Stock Price Movements from 2010–2024. The red dashed line represents the commonly accepted ‘good’ Sharpe Ratio threshold of 1.

Equation. 4: Formula for the Treynor Ratio, which quantifies the excess return earned by a portfolio per unit of systematic risk, as captured by its beta with respect to the market.

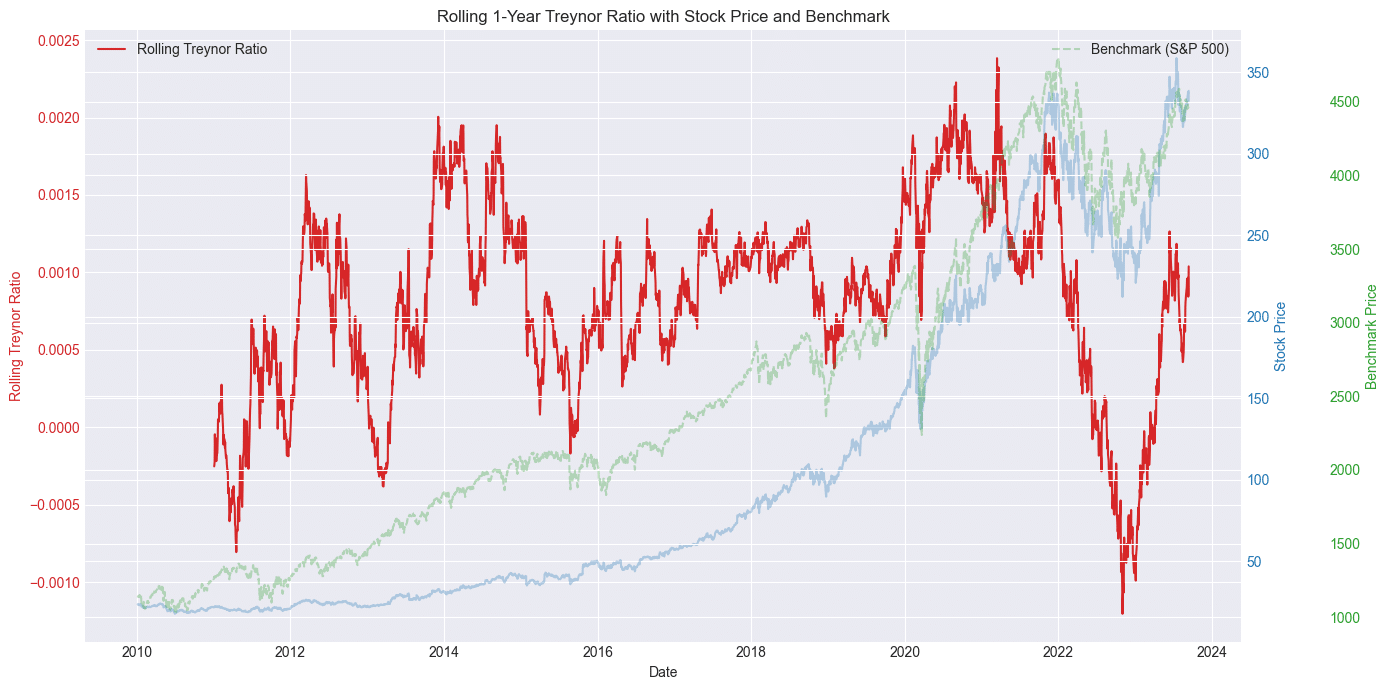

Figure. 3: Comparative Analysis of MSFT’s Performance (2010–2024): Rolling 1-Year Treynor Ratio juxtaposed against “MSFT” stock price and the S&P 500 benchmark. This visualization aids in evaluating risk-adjusted performance relative to market movements.

Equation. 5: Formula for the Treynor Ratio, which quantifies the excess return earned by a portfolio per unit of systematic risk, as captured by its beta with respect to the market.

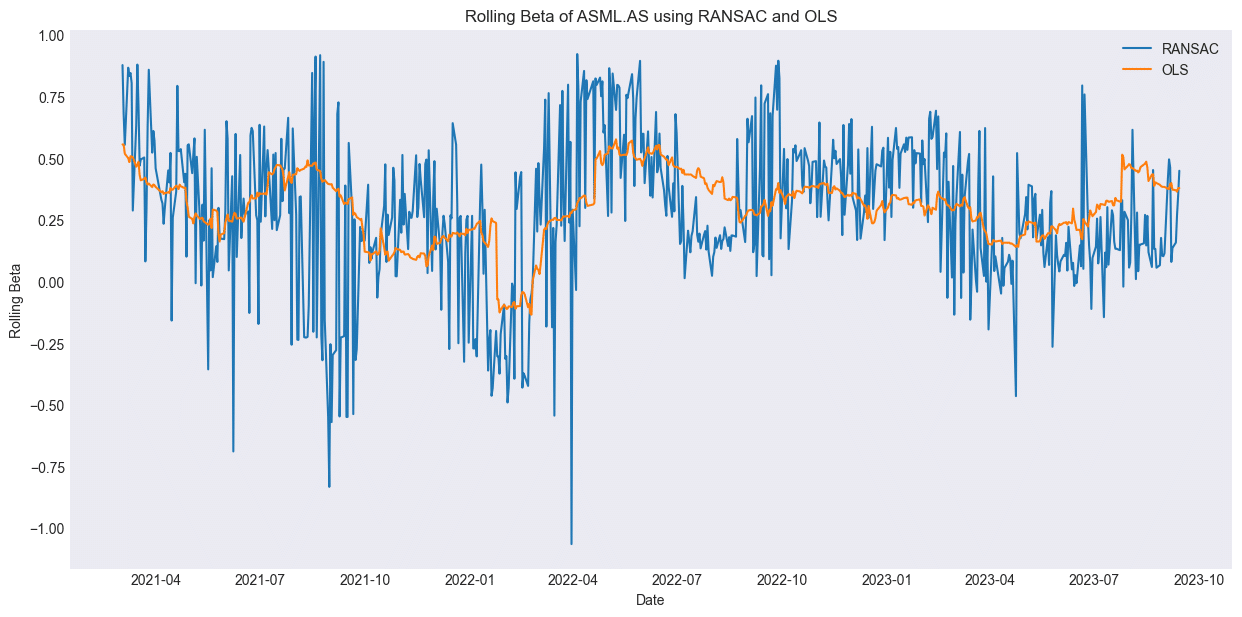

Figure. 4: Assessing Sensitivity to Market Fluctuations: Rolling Beta of “UNA.AS” (2016–2025) derived using both RANSAC and OLS methods. This comparative visualization offers insights into the stock’s responsiveness to broader market movements, highlighting potential anomalies and robustness in beta estimation.

Equation. 6: Formula for Jensen’s Alpha, which represents the abnormal return of a portfolio or security relative to the expected return predicted by the Capital Asset Pricing Model (CAPM). A positive Jensen’s Alpha indicates a strategy that has consistently beaten the market when adjusted for risk.

Newsletter