import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

# Get the stock data for ASML.AS

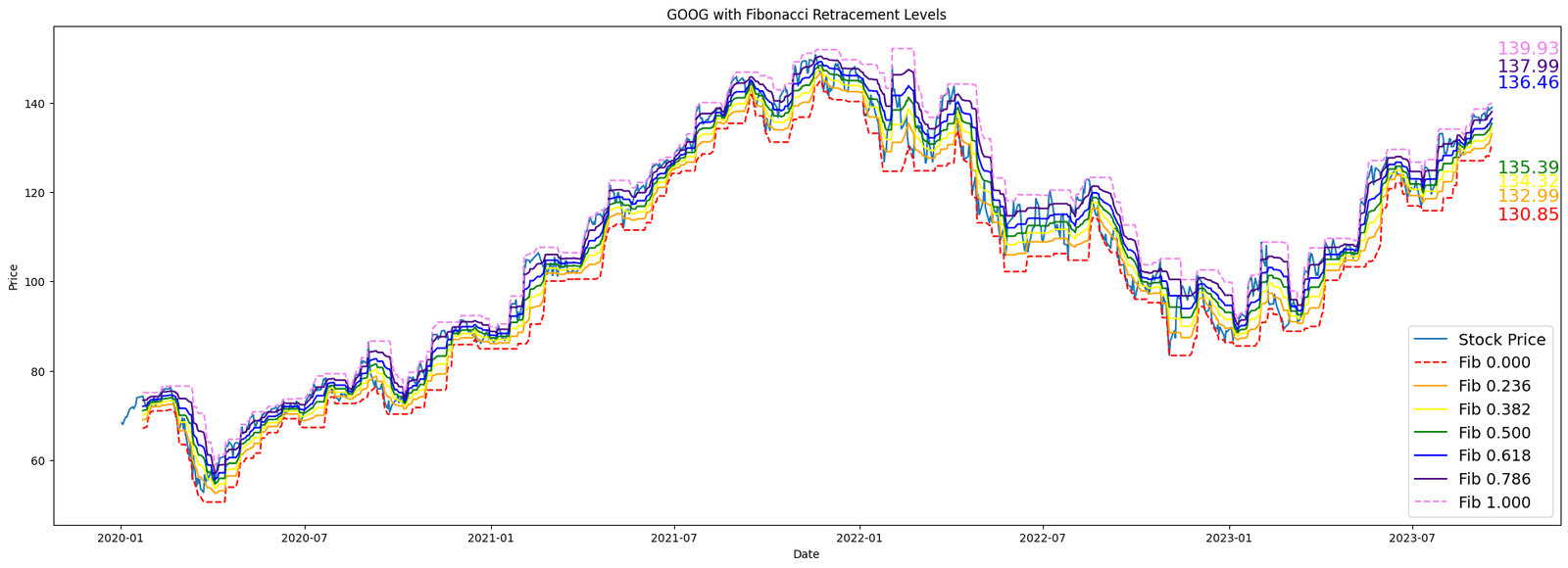

symbol = "GOOG"

stock_data = yf.download(symbol, start="2020-01-01", end="2023-12-17")

# Define the lookback period for calculating high and low prices

lookback_period = 15

# Calculate the high and low prices over the lookback period

high_prices = stock_data["High"].rolling(window=lookback_period).max()

low_prices = stock_data["Low"].rolling(window=lookback_period).min()

# Calculate the price difference and Fibonacci levels

price_diff = high_prices - low_prices

levels = np.array([0, 0.236, 0.382, 0.5, 0.618, 0.786, 1])

fib_levels = low_prices.values.reshape(-1, 1) + price_diff.values.reshape(-1, 1) * levels

# Get the last price for each Fibonacci level

last_prices = fib_levels[-1, :]

# Define a color palette for the Fibonacci levels

colors = ['red', 'orange', 'yellow', 'green', 'blue', 'indigo', 'violet']

# Plot the stock price with the Fibonacci retracement levels and last prices

fig, ax = plt.subplots(figsize=(24,8))

ax.plot(stock_data.index, stock_data["Close"], label="Stock Price")

offsets = [-16, -14, -12, -10, 8, 10, 12]

for i, level in enumerate(levels):

if level == 0 or level == 1:

linestyle = "--"

else:

linestyle = "-"

ax.plot(stock_data.index, fib_levels[:, i], label=f"Fib {level:.3f}", linestyle=linestyle, color=colors[i])

ax.annotate(f"{last_prices[i]:.2f}",

xy=(stock_data.index[-1], fib_levels[-1, i]),

xytext=(stock_data.index[-1] + pd.Timedelta(days=5), fib_levels[-1, i] + offsets[i]),

ha="left", va="center", fontsize=16, color=colors[i])

ax.set_xlabel("Date")

ax.set_ylabel("Price")

ax.set_title(f"{symbol} with Fibonacci Retracement Levels")

ax.legend(loc="lower right", fontsize=14)

plt.show()