import numpy as np

import pandas as pd

import yfinance as yf

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

plt.style.use("dark_background")

# USER PARAMETERS

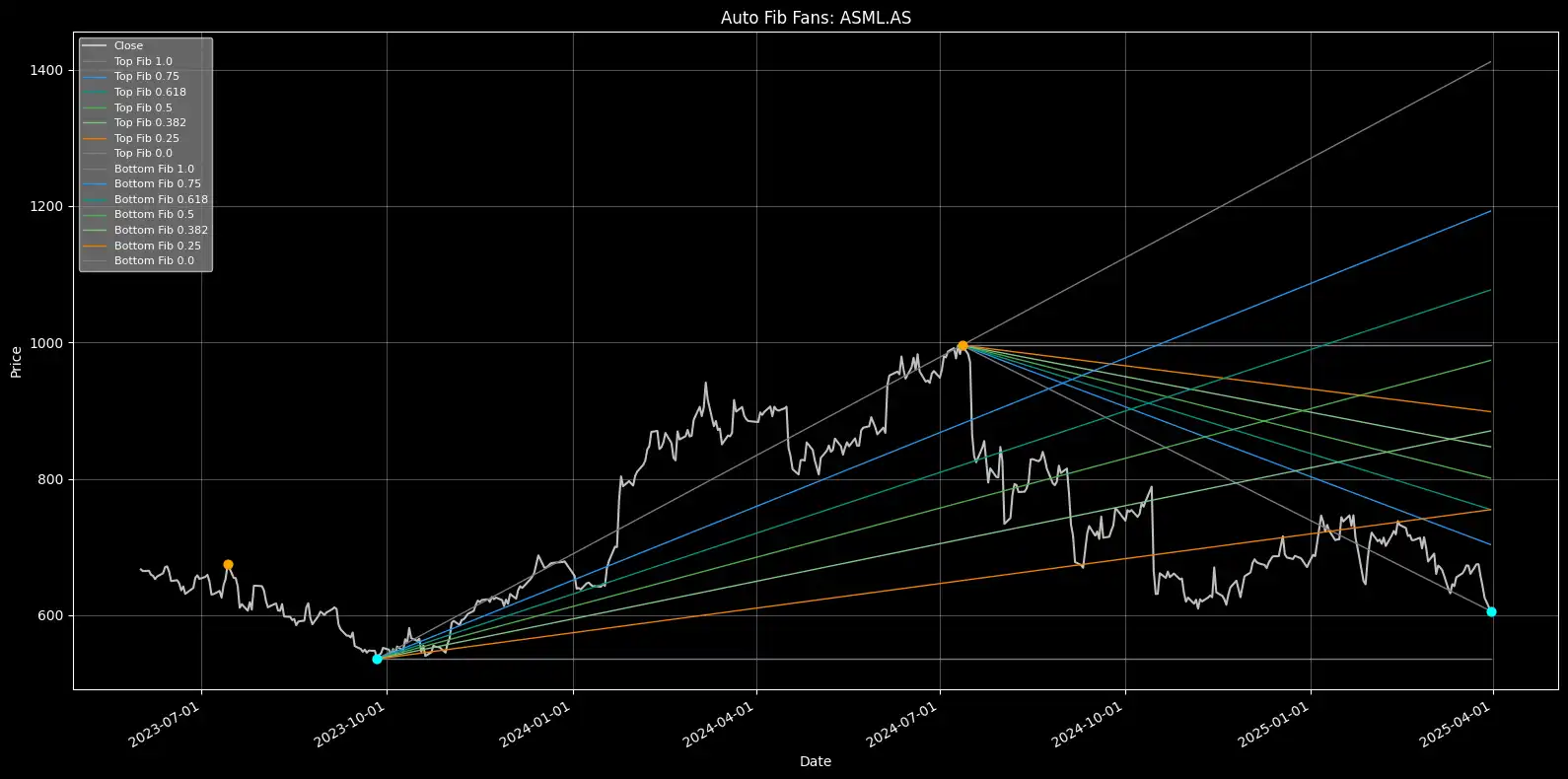

TICKER = "ASML.AS"

START_DATE = "2023-06-01"

END_DATE = "2026-03-01"

INTERVAL = "1d"

# How sensitive the pivot detection should be.

# Higher values = fewer pivots (only big moves count), lower values = more pivots.

DEVIATION_MULT = 3.0

# Fibonacci fan levels to plot (as ratios)

FIB_LEVELS = [1.0, 0.75, 0.618, 0.5, 0.382, 0.25, 0.0]

REVERSE_FANS = False # If True, the fan lines will be flipped (mirrored logic).

# Control whether to show top fans (from highs) and/or bottom fans (from lows).

draw_top_fans = True

draw_bottom_fans = True

# Choose which pivot the fan lines should start from.

# Example: if you set this to 1, the fan will start from the highest (or lowest) pivot found.

# Set to 2 if you want the second highest/lowest, and so on.

# This lets you control which swing point to use for drawing the fans.

top_origin_selection = 1

bottom_origin_selection = 1

# FIB COLORS

fib_colors = {

1.0: "#787b86",

0.75: "#2196f3",

0.618: "#009688",

0.5: "#4caf50",

0.382: "#81c784",

0.25: "#f57c00",

0.0: "#787b86"

}