import pandas as pd

import matplotlib.pyplot as plt

from pandas_datareader.data import get_data_fred

from datetime import datetime

# Define the start and end dates for the data

start_date = datetime(2023, 1, 1) # Start date for data retrieval

end_date = datetime(2025, 6, 30) # End date for data retrieval

# Retrieve the data for the yield curve

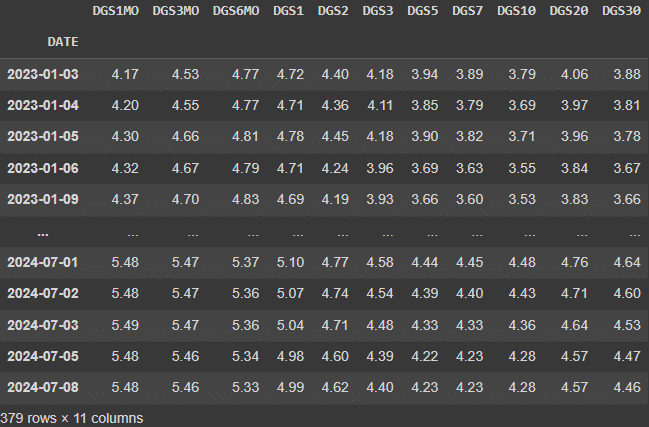

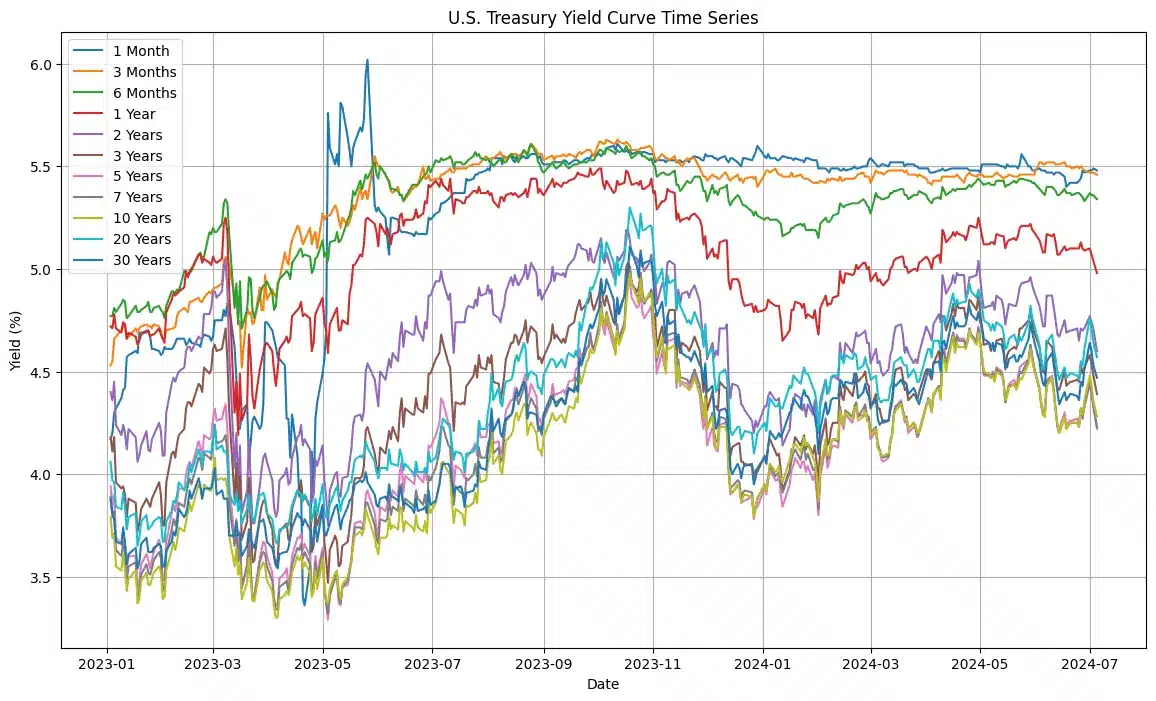

tickers = ['DGS1MO', 'DGS3MO', 'DGS6MO', 'DGS1', 'DGS2', 'DGS3', 'DGS5', 'DGS7', 'DGS10', 'DGS20', 'DGS30']

labels = {

'DGS1MO': '1 Month',

'DGS3MO': '3 Months',

'DGS6MO': '6 Months',

'DGS1': '1 Year',

'DGS2': '2 Years',

'DGS3': '3 Years',

'DGS5': '5 Years',

'DGS7': '7 Years',

'DGS10': '10 Years',

'DGS20': '20 Years',

'DGS30': '30 Years'

}

# Fetch yield data from FRED for the specified tickers and date range

yield_data = get_data_fred(tickers, start=start_date, end=end_date)

# Drop rows with missing values to clean the data

yield_data = yield_data.dropna()