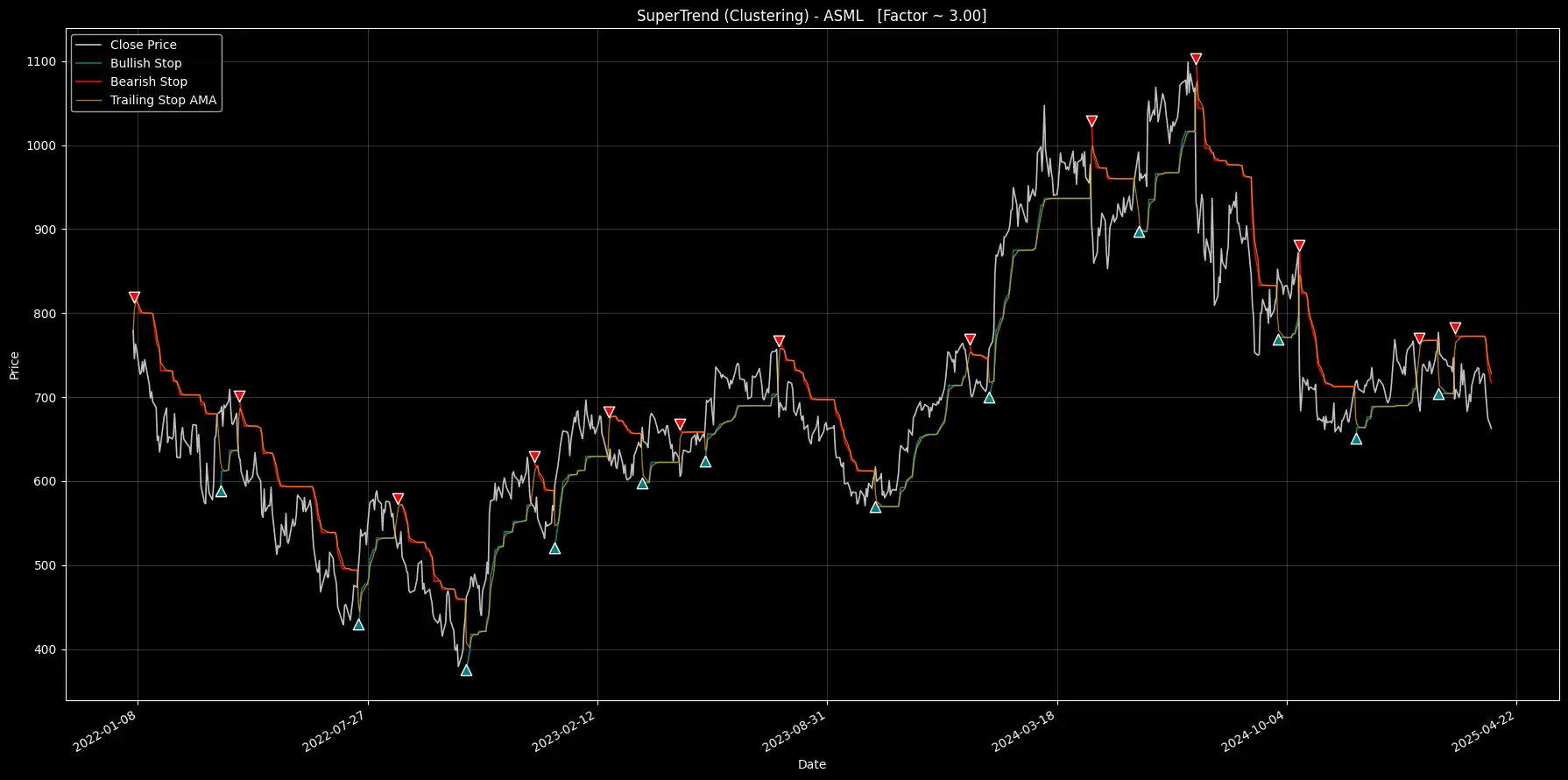

Trading Signals with Adaptive SuperTrend and K-Means

Figure 1. Architecture Diagram: Trading Signals with Adaptive SuperTrend and K-Means Clustering

Newsletter

Get Every Weekly Update & Insights

[mc4wp_form id=]

One thought on “Trading Signals with Adaptive SuperTrend and K-Means”

will you help me to implement it