import yfinance as yf

import matplotlib.pyplot as plt

import pandas as pd

import numpy as np

# Fetch stock data

def fetch_data(stock_symbol, start_date, end_date):

data = yf.download(stock_symbol, start=start_date, end=end_date)

return data

# SMA Function

def SMA(data, window):

return data.rolling(window=window).mean()

# EMA Function

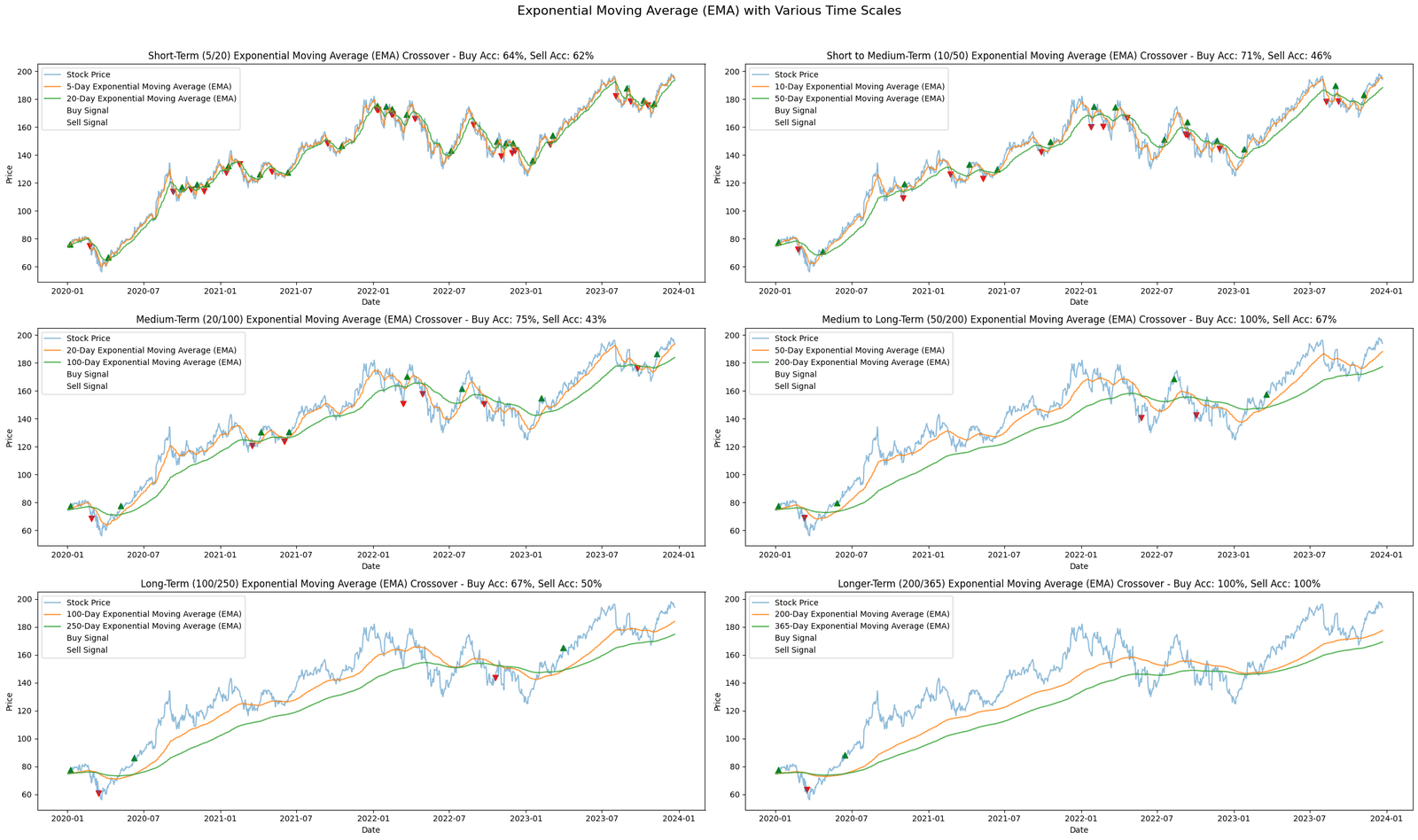

def EMA(data, window):

return data.ewm(span=window, adjust=False).mean()

# WMA Function

def WMA(data, window):

weights = np.arange(1, window + 1)

return data.rolling(window=window).apply(lambda prices: np.dot(prices, weights[::-1])/weights.sum(), raw=True)

# Identify buy and sell signals

def identify_signals(data, short_window, long_window, ma_function):

data['Short_MA'] = ma_function(data['Close'], short_window)

data['Long_MA'] = ma_function(data['Close'], long_window)

data['Signal'] = 0

data['Signal'] = np.where(data['Short_MA'] > data['Long_MA'], 1.0, 0.0)

data['Positions'] = data['Signal'].diff()

return data

# Calculate accuracy

def calculate_accuracy(data):

data['Future_Close'] = data['Close'].shift(-5) # Looking 5 days ahead

buys = data[(data['Positions'] == 1) & (data['Close'] < data['Future_Close'])]

sells = data[(data['Positions'] == -1) & (data['Close'] > data['Future_Close'])]

buy_accuracy = len(buys) / len(data[data['Positions'] == 1]) if len(data[data['Positions'] == 1]) > 0 else np.nan

sell_accuracy = len(sells) / len(data[data['Positions'] == -1]) if len(data[data['Positions'] == -1]) > 0 else np.nan

return buy_accuracy, sell_accuracy

# Plotting Function for Moving Averages with signals

def plot_ma_signals(stock_data, combinations, ma_function, ma_label):

fig, axs = plt.subplots(3, 2, figsize=(25, 15))

fig.suptitle(f'{ma_label} with Various Time Scales', fontsize=16)

term_labels = {

(5, 20): "Short-Term (5/20)",

(10, 50): "Short to Medium-Term (10/50)",

(20, 100): "Medium-Term (20/100)",

(50, 200): "Medium to Long-Term (50/200)",

(100, 250): "Long-Term (100/250)",

(200, 365): "Longer-Term (200/365)"

}

for i, (short_window, long_window) in enumerate(combinations, 1):

data = identify_signals(stock_data.copy(), short_window, long_window, ma_function)

buy_accuracy, sell_accuracy = calculate_accuracy(data)

term_label = term_labels.get((short_window, long_window), f"{short_window}/{long_window}")

ax = axs[(i-1)//2, (i-1)%2]

ax.plot(data.index, data['Close'], label='Stock Price', alpha=0.5)

ax.plot(data.index, data['Short_MA'], label=f'{short_window}-Day {ma_label}', alpha=0.8)

ax.plot(data.index, data['Long_MA'], label=f'{long_window}-Day {ma_label}', alpha=0.8)

ax.scatter(data.index, data['Close'], label='Buy Signal', marker='^', color='g', alpha=1, s=50 * data['Positions'].clip(lower=0))

ax.scatter(data.index, data['Close'], label='Sell Signal', marker='v', color='r', alpha=1, s=50 * data['Positions'].clip(upper=0).abs())

accuracy_title = f"Buy Acc: {buy_accuracy*100:.0f}%, Sell Acc: {sell_accuracy*100:.0f}%"

ax.set_title(f'{term_label} {ma_label} Crossover - {accuracy_title}')

ax.set_xlabel('Date')

ax.set_ylabel('Price')

ax.legend()

plt.tight_layout(rect=[0, 0, 1, 0.96])

plt.show()

# Main Functions Execution

stock = 'AAPL'

start_date = '2020-01-01'

end_date = '2024-01-01'

time_scale_combinations = [(5, 20), (10, 50), (20, 100), (50, 200), (100, 250), (200, 365)]

stock_data = fetch_data(stock, start_date, end_date)

# Plot for SMA

plot_ma_signals(stock_data, time_scale_combinations, SMA, "Simple Moving Average (SMA)")

# Plot for EMA

plot_ma_signals(stock_data, time_scale_combinations, EMA, "Exponential Moving Average (EMA)")

# Plot for WMA

plot_ma_signals(stock_data, time_scale_combinations, WMA, "Weighted Moving Average (WMA)")