Optimize Portfolio Performance with Risk Parity Rebalancing in Python

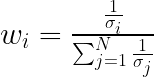

Equation. 1: The formula for calculating the inverse volatility weights in Risk Parity.

Figure. 1: Visualizing Risk Parity: as Individual stock risk contributions adjust dynamically, observe how the total portfolio volatility responds in tandem, showcasing the essence of risk balanced asset allocation.

Newsletter

Get Every Weekly Update & Insights

[mc4wp_form id=]