Identifying Today’s Stock Pattern in Historical Data Considering Current Market Conditions and Visualizing Future Movements in Python

Previously, we showed how Dynamic Time Warping (DTW) could be used in mining patterns from recurring price movements in stock data and how to leverage these patterns for predictive purposes.

However, price alone might not provide a sufficient view of current market conditions. In this article, we augment the idea with additional variables, enriching the representation of market dynamics in our pattern recognition framework.

The core of the pattern recognition method still relies on DTW but with a twist. Instead of just comparing the price data, we now also compare the technical indicators data between different windows.

To manage computational complexity, we use Principal Component Analysis (PCA). This reduces the dimensionality of indicator data into a manageable set of uncorrelated variables.

1. Methodology — PCA + DTW

The method combines PCA and DTW to not only for mining patterns purely related to price but to also bring technical indicators into the mix for a more comprehensive technique.

First, we’ll very briefly go over each technique on its own, i.e. PCA and DTW, and then explore how they come together in the framework to help identify patterns in stock price data.

1.1 Principal Component Analysis

PCA is a statistical technique used for dimensionality reduction, which is very valuable when navigating through a high-dimensional space of data, in this case, technical indicators.

It works by identifying the “principal components” that capture the most variance within the data, thus encapsulating the essential information in a reduced-dimensional space.

One way to think about PCA is that it helps to reduce the number of variables into a few variables that capture most of the variance and are uncorrelated with one another.

We will not dive too much into the inner workings of PCA, but there is a wealth of material available online for those interested in a deeper understanding.

1.2 Dynamic Time Warping

DTW is a method used for measuring the similarity between two temporal sequences, i.e. time series, which may vary in length. DTW aligns sequences in a time-warped manner, allowing for a more nuanced comparison. The DTW distance formula is given by

Equation 1. The DTW distance between two time series A and B of potentially unequal length. ai and bj(i) denote the elements of A and B at arbitrary indices i and j(i) respectively. DTW allows for optimal alignment between the points of the two time series, thereby enabling a more flexible measure of similarity.

In our context, it serves as a tool for comparing price movements over specific time frames. And the methodology could be expanded even when the price movements are of differing lengths.

1.3 Pattern Recognition Method

The aim is to mine patterns in a designated “current window” of price data by comparing it with numerous “past windows” from the historical data. Furhtermore, these windows encapsulate a specified number of days, and the process is iterated for different window sizes to identify patterns across various time frames.

For each window, we perform a dual comparison using DTW. We compare the price data and the PCA-reduced technical indicators data. We compute a composite distance measure for each past window against the current window, incorporating both the price data and the technical indicators data.

1.4 Weighting Scheme: PCA vs DTW

We introduce a weight parameter to serve as a fulcrum, balancing the emphasis between the price data and the technical indicators data. Moreover, by tweaking this parameter, the methodology can be tuned to lean more toward either of the two data sources.

Equation 2. The formula shows the weighted distance computation, where D is the combined DTW distance, Dreturns and Dindicators are the DTW distances from percentage change and PCA Reduced indicator features respectively, and ω is the weighting factor.

In our context, it serves as a tool for comparing price movements over specific time frames. And the methodology could be expanded even when the price movements are of differing lengths.

1.5 Mining Patterns in the Historical Data

The objective for mining patterns is to identify past windows that show a low composite distance to the current window, indicating high similarity. The lower the distance, the more analogous the patterns become.

The three to five most similar past windows are then retrieved and visualized, and their subsequent price movements are analyzed to project a median subsequent price path for the current window.

Figure. 1: The method Pattern Recognition Method using PCA and DTW segments recent price data into a ‘current window’ and compares it to historical data windows of the same size, identifying and ranking the most similar patterns for different window sizes.

2. Implementation in Python

2.1 Importing Necessary Libraries

The libraries required include pandas, numpy, and matplotlib for data manipulation and visualization, yfinance for fetching stock price data, fastdtw for DTW implementation, scipy for distance computation, ta for technical analysis, sklearn for PCA and data imputation.

2.2 Adding Technical Indicators

Next, we define a function to compute and add various technical indicators to the stock price data. Technical indicators are included as demonstration purposes. Any set of ‘explanatory’ variables can be included here.

def add_ta_features(data):

# function to add technical indicators

# ...

return data

2.3 Data Normalization

Normalization is a crucial step to ensure that the data is on a similar scale. Define a function to normalize the time-series data.

def normalize(ts):

return (ts - ts.min()) / (ts.max() - ts.min())

2.4 Dynamic Time Warping Distance Calculation

We define a function to calculate the DTW distance. It uses a weighting scheme to balance price changes and technical indicators in our methodology.

Moreover, higher values would prioritize patterns closely aligned with price movements, while lower values would favor matches more reflective of the indicators used.

def dtw_distance(ts1, ts2, ts1_ta, ts2_ta, weight=0.75): # Adjust the weight parameter as needed

ts1_normalized = normalize(ts1)

ts2_normalized = normalize(ts2)

distance_pct_change, _ = fastdtw(ts1_normalized.reshape(-1, 1), ts2_normalized.reshape(-1, 1), dist=euclidean)

distance_ta, _ = fastdtw(ts1_ta, ts2_ta, dist=euclidean)

distance = weight * distance_pct_change + (1 - weight) * distance_ta

return distance

2.5 Feature Reduction using PCA

Before employing DTW, we reduce the dimensionality of the technical indicator data using PCA with this function.

def extract_and_reduce_features(data, n_components=3):

ta_features = data.drop(columns=['Open', 'High', 'Low', 'Close', 'Volume', 'Adj Close'])

# Impute missing values

imputer = SimpleImputer(strategy='mean')

imputed_ta_features = imputer.fit_transform(ta_features)

pca = PCA(n_components=n_components)

reduced_features = pca.fit_transform(imputed_ta_features)

return reduced_features

2.6 Fetching Data and Pre-processing

The next step is to fetch the stock price data, add technical indicators, reduce the features using PCA, and compute the percentage change in closing prices.

ticker = "ASML.AS"

start_date = '2000-01-01'

end_date = '2023-05-01'

data = yf.download(ticker, start=start_date, end=end_date)

data_with_ta = add_ta_features(data)

reduced_features = extract_and_reduce_features(data_with_ta, n_components=3)

price_data_pct_change = data_with_ta['Close'].pct_change().dropna()

2.7 Complete Code

This involves iterating through data, calculating DTW distances, identifying similar patterns, and visualizing findings.

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from fastdtw import fastdtw

from scipy.spatial.distance import euclidean

import ta

from sklearn.decomposition import PCA

from sklearn.impute import SimpleImputer

def add_ta_features(data):

# Add Trend indicators

data['trend_ichimoku_conv'] = ta.trend.ichimoku_a(data['High'], data['Low'])

data['trend_ema_slow'] = ta.trend.ema_indicator(data['Close'], 50)

data['momentum_kama'] = ta.momentum.kama(data['Close'])

data['trend_psar_up'] = ta.trend.psar_up(data['High'], data['Low'], data['Close'])

data['volume_vwap'] = ta.volume.VolumeWeightedAveragePrice(data['High'], data['Low'], data['Close'], data['Volume']).volume_weighted_average_price()

data['trend_ichimoku_a'] = ta.trend.ichimoku_a(data['High'], data['Low'])

data['volatility_kcl'] = ta.volatility.KeltnerChannel(data['High'], data['Low'], data['Close']).keltner_channel_lband()

data['trend_ichimoku_b'] = ta.trend.ichimoku_b(data['High'], data['Low'])

data['trend_ichimoku_base'] = ta.trend.ichimoku_base_line(data['High'], data['Low'])

data['trend_sma_fast'] = ta.trend.sma_indicator(data['Close'], 20)

data['volatility_dcm'] = ta.volatility.DonchianChannel(data['High'], data['Low'], data['Close']).donchian_channel_mband()

data['volatility_bbl'] = ta.volatility.BollingerBands(data['Close']).bollinger_lband()

data['volatility_bbm'] = ta.volatility.BollingerBands(data['Close']).bollinger_mavg()

data['volatility_kcc'] = ta.volatility.KeltnerChannel(data['High'], data['Low'], data['Close']).keltner_channel_mband()

data['volatility_kch'] = ta.volatility.KeltnerChannel(data['High'], data['Low'], data['Close']).keltner_channel_hband()

data['trend_sma_slow'] = ta.trend.sma_indicator(data['Close'], 200)

data['trend_ema_fast'] = ta.trend.ema_indicator(data['Close'], 20)

data['volatility_dch'] = ta.volatility.DonchianChannel(data['High'], data['Low'], data['Close']).donchian_channel_hband()

data['others_cr'] = ta.others.cumulative_return(data['Close'])

data['Adj Close'] = data['Close']

return data

def normalize(ts):

return (ts - ts.min()) / (ts.max() - ts.min())

def dtw_distance(ts1, ts2, ts1_ta, ts2_ta, weight=0.75): # Adjust the weight parameter as needed

ts1_normalized = normalize(ts1)

ts2_normalized = normalize(ts2)

distance_pct_change, _ = fastdtw(ts1_normalized.reshape(-1, 1), ts2_normalized.reshape(-1, 1), dist=euclidean)

distance_ta, _ = fastdtw(ts1_ta, ts2_ta, dist=euclidean)

distance = weight * distance_pct_change + (1 - weight) * distance_ta

return distance

def extract_and_reduce_features(data, n_components=3):

ta_features = data.drop(columns=['Open', 'High', 'Low', 'Close', 'Volume', 'Adj Close'])

# Impute missing values

imputer = SimpleImputer(strategy='mean')

imputed_ta_features = imputer.fit_transform(ta_features)

pca = PCA(n_components=n_components)

reduced_features = pca.fit_transform(imputed_ta_features)

return reduced_features

ticker = "ASML.AS"

start_date = '2000-01-01'

end_date = '2023-05-01'

data = yf.download(ticker, start=start_date, end=end_date)

data_with_ta = add_ta_features(data)

reduced_features = extract_and_reduce_features(data_with_ta, n_components=3)

price_data_pct_change = data_with_ta['Close'].pct_change().dropna()

subsequent_days = 15

days_to =[15, 20, 30]

min_gap = 10 # Set a minimum gap of 10 days between patterns found

for n_days in days_to:

current_window = price_data_pct_change[-n_days:].values

current_ta_window = reduced_features[-n_days:]

# Initialize distances with inf

distances = [np.inf] * (len(price_data_pct_change) - 2 * n_days - subsequent_days)

for start_index in range(len(price_data_pct_change) - 2 * n_days - subsequent_days):

# Ensure there is a minimum gap before or after the current window

gap_before = len(price_data_pct_change) - (start_index + n_days + subsequent_days)

gap_after = start_index - (len(price_data_pct_change) - n_days)

if gap_before >= min_gap or gap_after >= min_gap:

distances[start_index] = dtw_distance(

current_window,

price_data_pct_change[start_index:start_index + n_days].values,

current_ta_window,

reduced_features[start_index:start_index + n_days]

)

min_distance_indices = np.argsort(distances)[:3] # find indices of 3 smallest distances

fig, axs = plt.subplots(1, 2, figsize=(30, 8))

# plot the entire stock price data

axs[0].plot(data['Close'], color='blue', label='Overall stock price')

for i, start_index in enumerate(min_distance_indices):

# plot the pattern period in different colors

past_window_start_date = data.index[start_index]

past_window_end_date = data.index[start_index + n_days + subsequent_days]

axs[0].plot(data['Close'][past_window_start_date:past_window_end_date], color='C{}'.format(i), label=f"Pattern {i + 1}")

axs[0].set_title(f'{ticker} Stock Price Data')

axs[0].set_xlabel('Date')

axs[0].set_ylabel('Stock Price')

axs[0].legend()

# plot the reindexed patterns

for i, start_index in enumerate(min_distance_indices):

past_window = price_data_pct_change[start_index:start_index + n_days + subsequent_days]

reindexed_past_window = (past_window + 1).cumprod() * 100

axs[1].plot(range(n_days + subsequent_days), reindexed_past_window, color='C{}'.format(i), linewidth=3 if i == 0 else 1, label=f"Past window {i + 1} (with subsequent {subsequent_days} days)")

reindexed_current_window = (price_data_pct_change[-n_days:] + 1).cumprod() * 100

axs[1].plot(range(n_days), reindexed_current_window, color='k', linewidth=3, label="Current window")

# Collect the subsequent prices of the similar patterns

subsequent_prices = []

for i, start_index in enumerate(min_distance_indices):

subsequent_window = price_data_pct_change[start_index + n_days : start_index + n_days + subsequent_days].values

subsequent_prices.append(subsequent_window)

subsequent_prices = np.array(subsequent_prices)

median_subsequent_prices = np.median(subsequent_prices, axis=0)

# Adjusted line for reindexing the median subsequent prices

median_subsequent_prices_cum = (median_subsequent_prices + 1).cumprod() * reindexed_current_window.iloc[-1]

axs[1].plot(range(n_days, n_days + subsequent_days), median_subsequent_prices_cum, color='grey', linestyle='dashed', label="Median Subsequent Price Estimation")

axs[1].set_title(f"Most similar {n_days}-day patterns in {ticker} stock price history (aligned, reindexed)")

axs[1].set_xlabel("Days")

axs[1].set_ylabel("Reindexed Price")

axs[1].legend()

#plt.savefig(f'{ticker}_{n_days}_days.png')

#plt.close(fig)

plt.show()

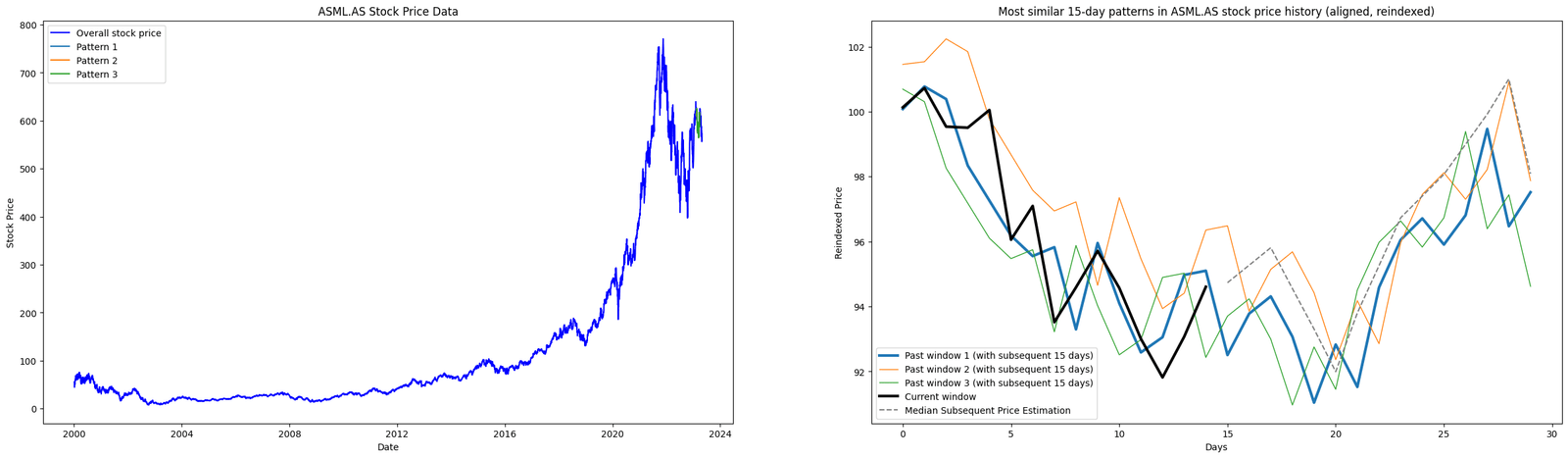

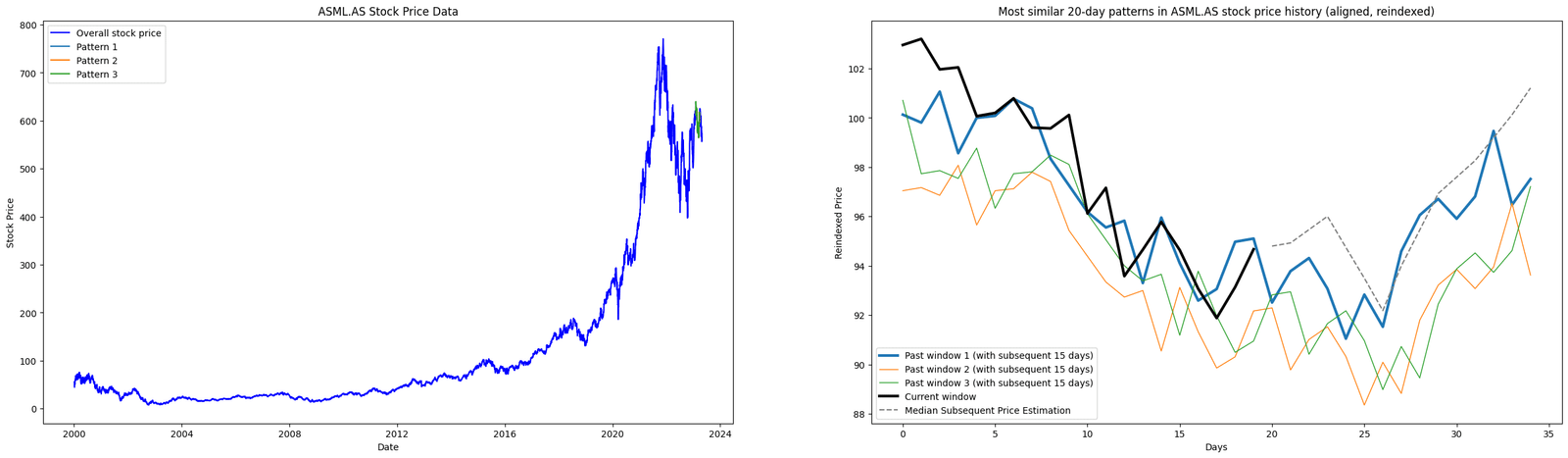

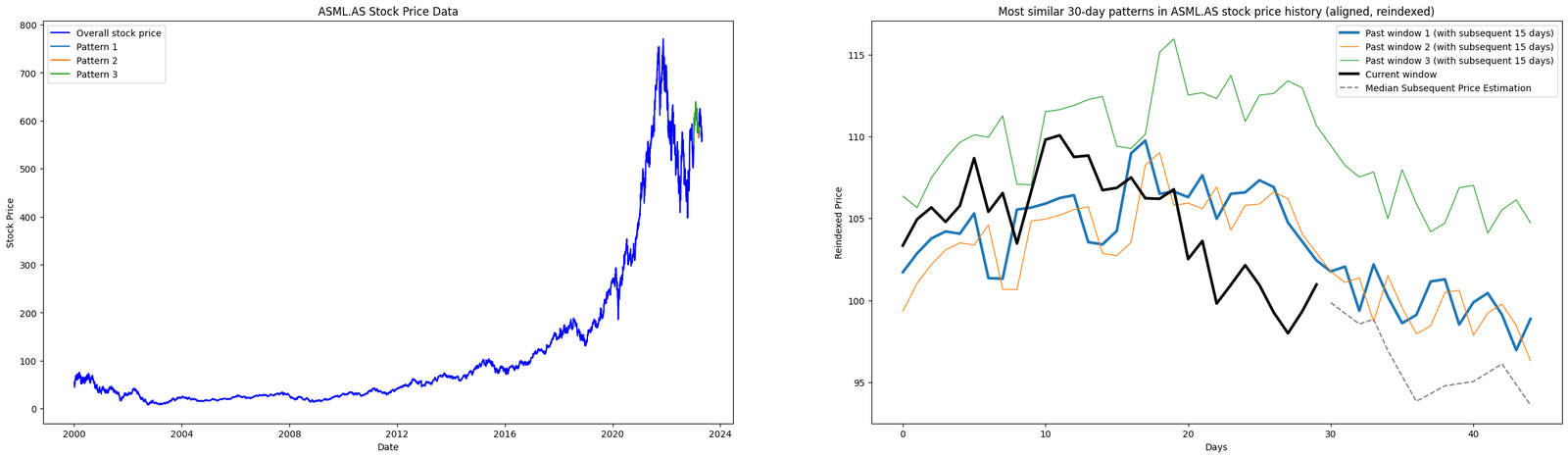

Figure. 2: Leveraging DTW and PCA: The visualization examines various window periods (15, 20, and 30 days) to identify and compare past pricing patterns in ASML.AS stock data with recent patterns. The plots display overall price data and reindexed, normalized patterns. They highlight three past instances with the closest resemblance in temporal dynamics.

3. Interpretation of Results

3.1 Top Patterns Identified

The core objective of this analysis is to use historical price patterns to predict future stock price trajectories. We used PCA and DTW to mine patterns and identify similar past price movements in the stock data.

Furthermore, the code identifies and visualizes the top three historical stock price patterns, ranking them from most to least similar.

The code compares a recent price pattern with historical data, ranking the top three similar past patterns. These are visualized next to the recent pattern, showing price movements after those patterns.

Lastly. the code then estimates potential future prices based on a median price trajectory derived from these similar past patterns.

3.1 Accuracy of the Results

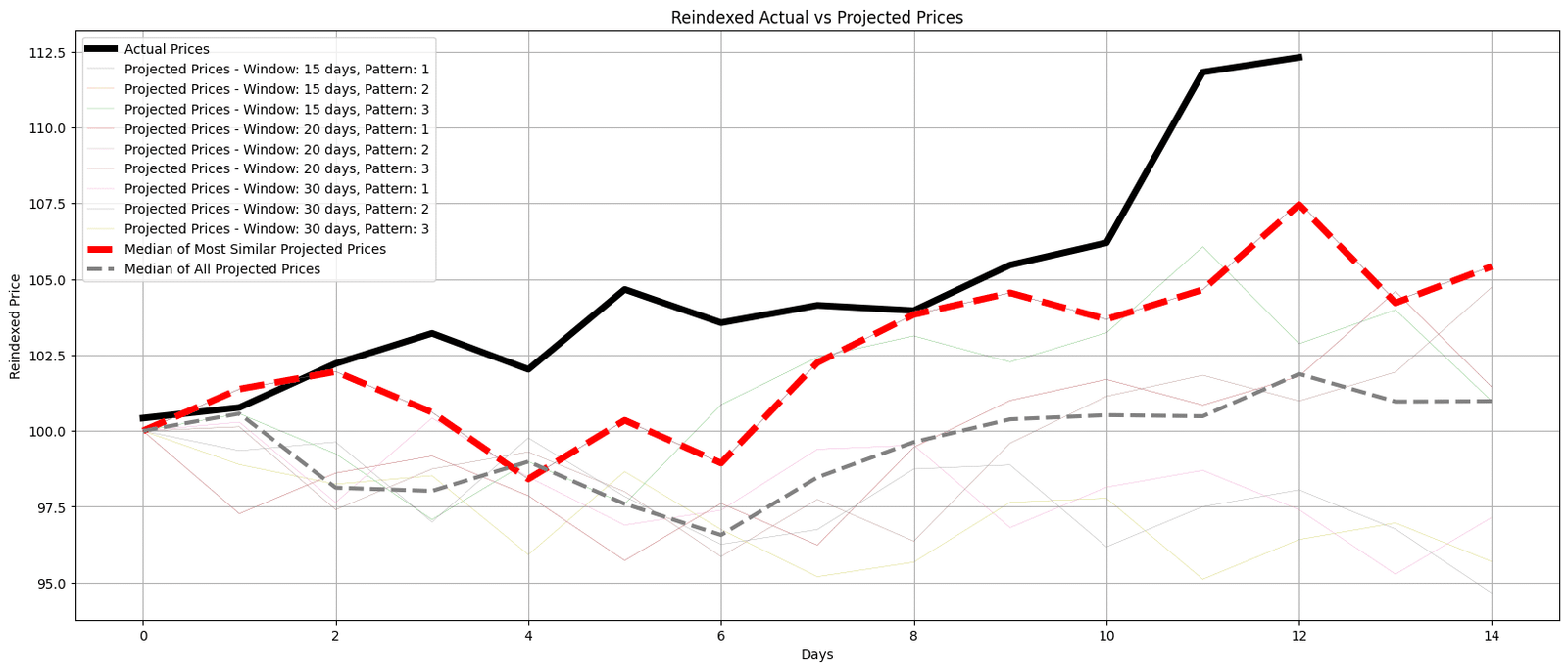

In the chart below, we explore the accuracy of all the patterns found in each window. The black line represents actual recent prices, while the colored lines depict the projected prices based on past patterns for different window sizes.

Additionally, two dashed lines, red and grey, show medians for the most similar and all projected prices respectively, offering a consolidated view.

This visual representation hypothesizes future stock price behavior based on historical patterns.

The overlap, divergence, and trends of actual and median projected prices illustrate the method’s strengths and limitations.

Figure. 3: This graph contrasts reindexed actual prices with projections from historical patterns. A red dashed line shows the median of the most similar projected prices. A grey dashed line represents the median of all projected prices, highlighting the method’s accuracy and predictive range.

4. Limitations and Improvements

This is the initial step in using DTW and PCA to mine stock price patterns. There are limitations and areas for improvement to consider.

4.1 Limitations

4.1.1. Optimization of Parameter through Backtesting

The performance of DTW and PCA largely depends on parameter choices like the weighting factor, window sizes, and PCA variables. Currently, there is no systematic approach for tuning these parameters.

Incorporating techniques like grid search or evolutionary algorithms could optimize parameters, enhancing the accuracy and reliability of our methodology.

4.1.2. Assumption of Repeating Patterns

The core assumption that past price patterns will reoccur in the future is a common simplification, yet it’s not always valid. Market dynamics evolve, and historical patterns may not necessarily repeat or lead to accurate projections.

4.2 Further Improvements

4.2.1. Incorporation of Additional Predictive Indicators

Adding diverse predictive indicators or alternative data sources could enhance the accuracy of our pattern recognition methodology.

4.2.2. Statistical Validation of Patterns

An improvement could be making sure the patterns found are truly similar, not just by looking, but using a statistical test like a t-test. This test helps us see if the patterns we find in historical data are statistically similar to the current pattern or if they just look alike by chance.

4.2.3. Robustness Against Market Anomalies

Designing mechanisms to address price anomalies or extreme events could improve the resilience and accuracy of our methodology. One way to smoothen out anomalies is through moving average methods.

4.2.4. Cross-Asset Pattern Recognition

Expanding the scope to include similar assets or even different markets could also provide a richer analysis. Exploring related assets or sectors can reveal broader market trends.

5. Concluding Thoughts

We’ve taken some first steps towards a new way of mining patterns in stock prices. With DTW and PCA, we’ve started to sketch out a method that could help spot repeating patterns in historical stock data.

However, this is just a starting point. There are several areas we identified that need improvement, and the method needs to be tested more rigorously to see how well it really works.

Pattern Mining for Stock Prediction with Dynamic Time Warping

Newsletter