Finding Mispriced Stocks with a 6 Factor Model

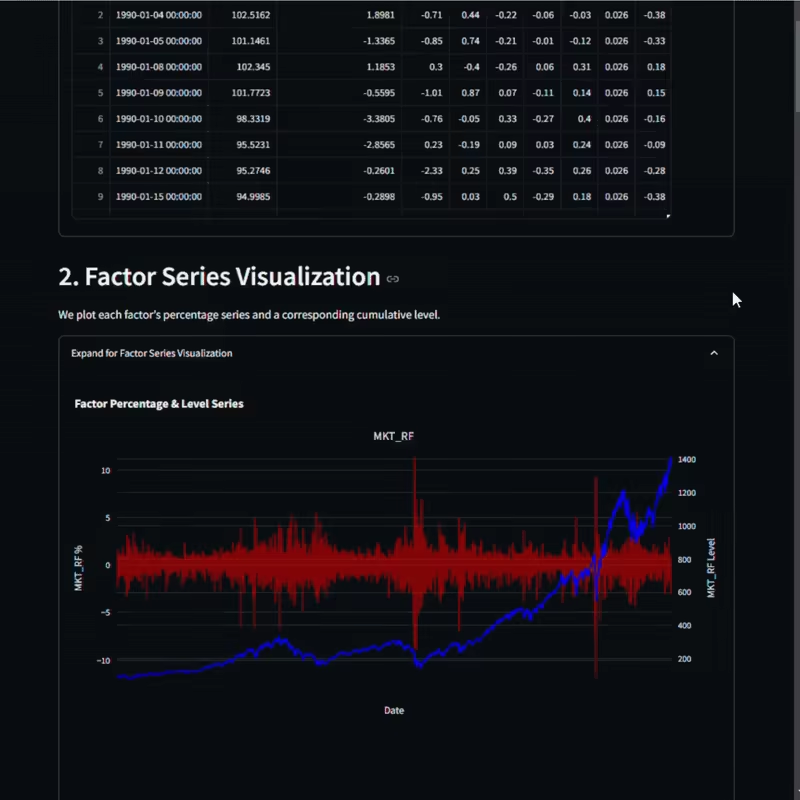

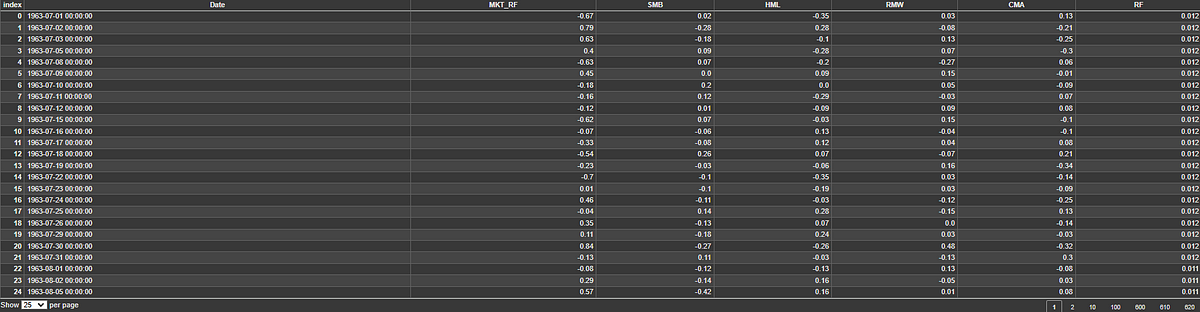

Figure 1: Fama-French factor data, including market risk (MKT_RF), size (SMB), value (HML), profitability (RMW), investment (CMA), and risk-free rate (RF).

Newsletter

Get Every Weekly Update & Insights

[mc4wp_form id=]