Analyzing Rolling Z-Score in Stock Trading with Python

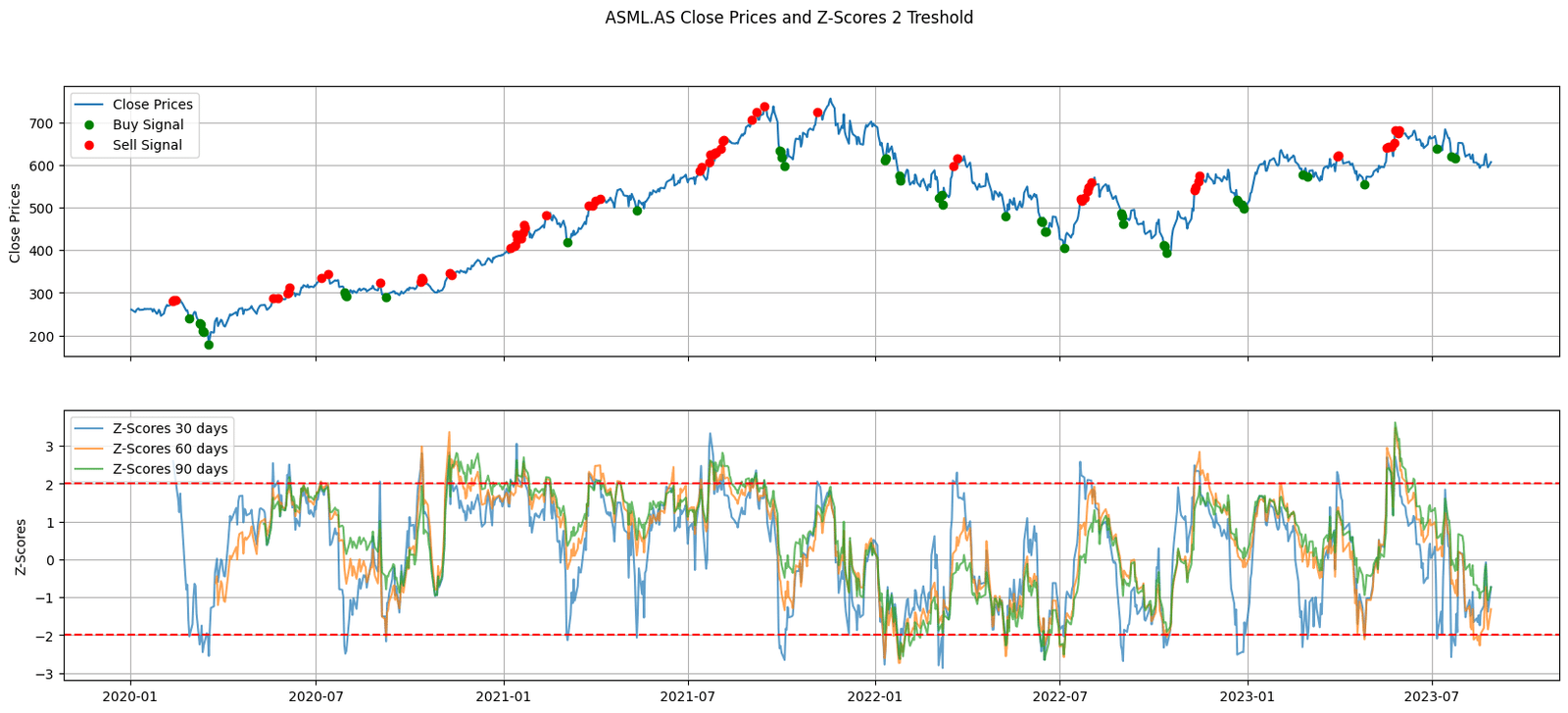

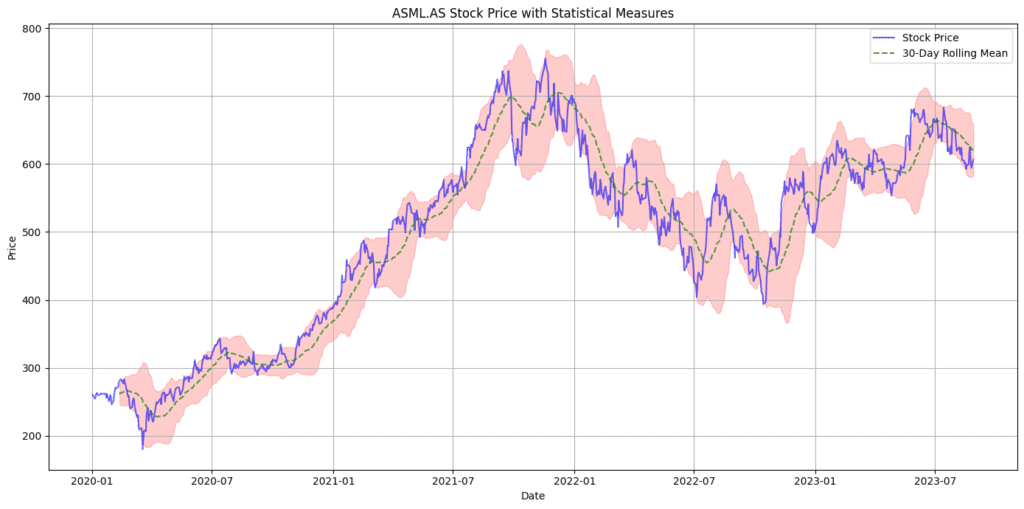

Figure 1. Evolution of ASML.AS stock prices juxtaposed with rolling Z-Scores over 30, 60, and 90-day periods. Green and red markers highlight potential buy and sell points respectively, based on Z-Score thresholds.

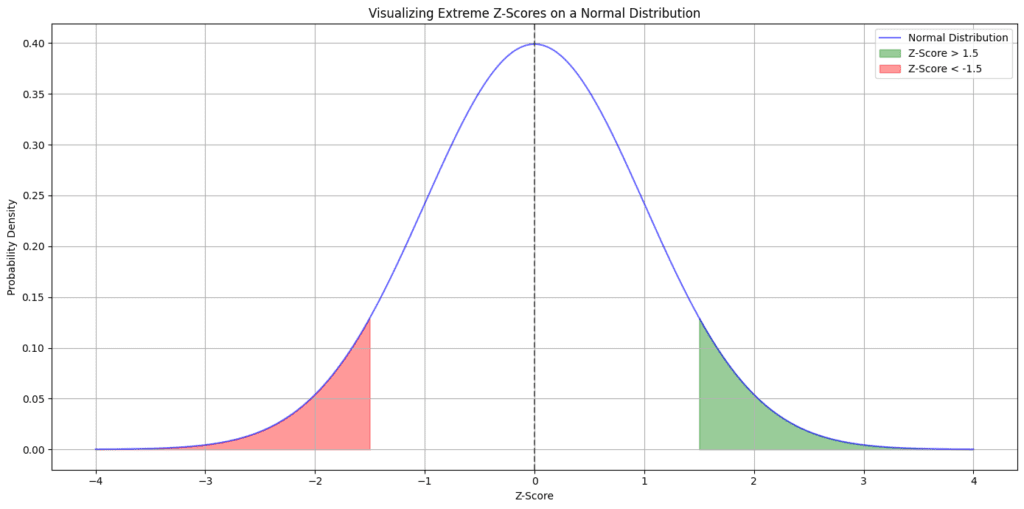

Equation. 1: The Z-Score Formula: A mathematical representation detailing how deviations from the mean are standardized using the population’s standard deviation. This equation is pivotal for traders aiming to quantify stock price movements relative to historical data.

Newsletter

Get Every Weekly Update & Insights

[mc4wp_form id=]