import warnings

warnings.filterwarnings('ignore')

import numpy as np

import pandas as pd

import yfinance as yf

import matplotlib.pyplot as plt

from matplotlib.dates import MonthLocator, DateFormatter

# 1. Download data

tickers = ['^VIX', '^GSPC']

start, end = '2015-01-01', '2025-07-02'

raw = yf.download(

tickers,

start=start,

end=end,

progress=False,

auto_adjust=False

)

# 2. Extract series

vix = raw['Close']['^VIX']

spx = raw['Close']['^GSPC']

# 3. Flatten columns

if isinstance(raw.columns, pd.MultiIndex):

raw.columns = raw.columns.get_level_values(0)

df = raw.copy()

df.columns = df.columns.map(str.title)

# 4. Compute 21-day realized volatility

window = 21

daily_ret = np.log(spx).diff()

real_vol = daily_ret.rolling(window).std() * np.sqrt(252)

real_vol = real_vol.dropna()

# 5. Align VIX to realized-vol dates

vix = vix.loc[real_vol.index]

# 6. Scale realized vol and compute difference

scale = vix.mean() / real_vol.mean()

real_scaled = real_vol * scale

diff = vix - real_scaled

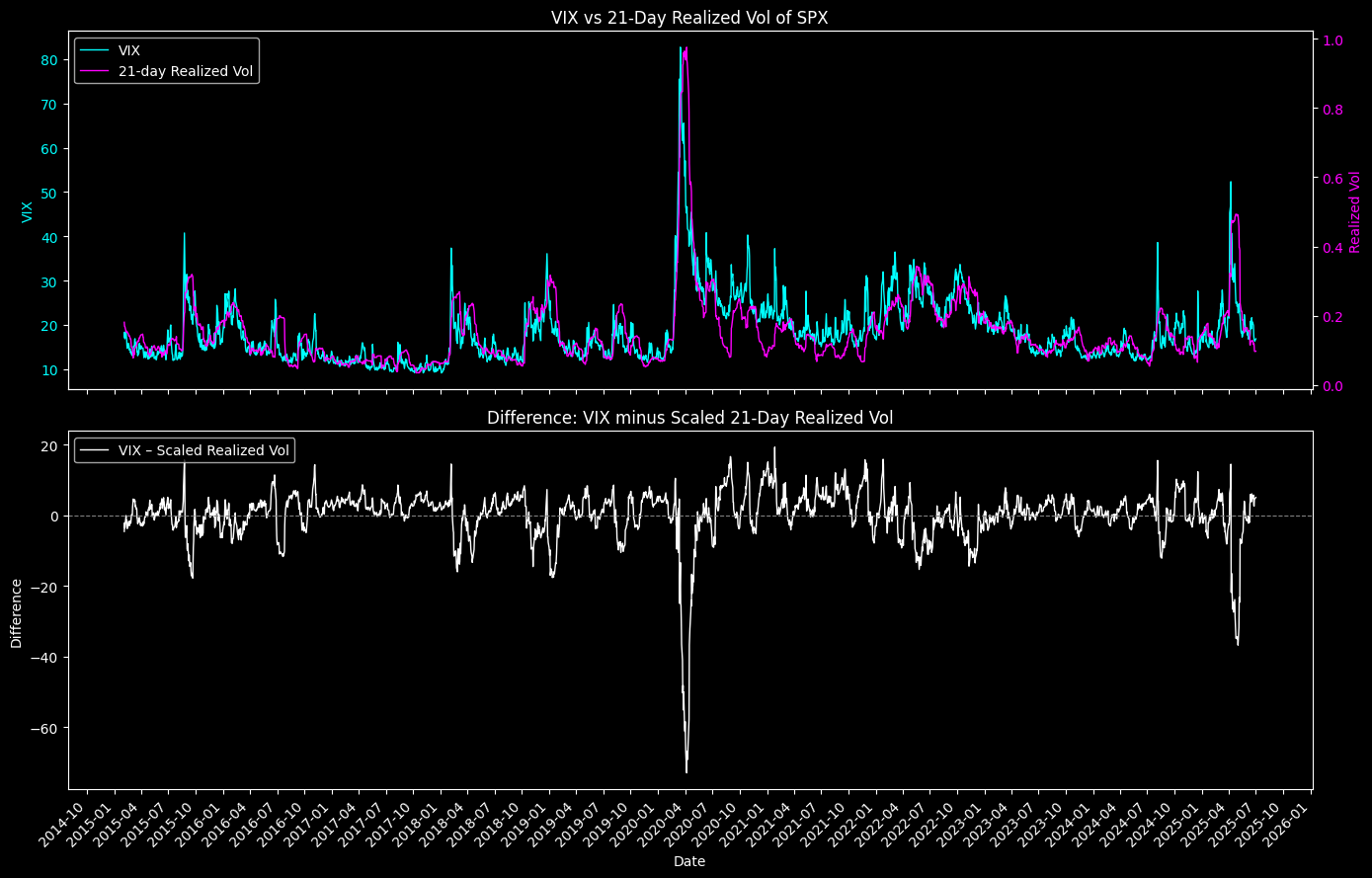

# 7. Plot both charts as subplots

plt.style.use('dark_background')

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(14, 9), sharex=True)

# Subplot 1: VIX vs Realized Vol

ax1.plot(vix.index, vix, color='cyan', linewidth=1, label='VIX')

ax1.set_ylabel('VIX', color='cyan')

ax1.tick_params(axis='y', labelcolor='cyan')

ax1b = ax1.twinx()

ax1b.plot(real_vol.index, real_vol,

color='magenta', linewidth=1,

label=f'{window}-day Realized Vol')

ax1b.set_ylabel('Realized Vol', color='magenta')

ax1b.tick_params(axis='y', labelcolor='magenta')

lines1, labs1 = ax1.get_legend_handles_labels()

lines1b, labs1b = ax1b.get_legend_handles_labels()

ax1.legend(lines1 + lines1b, labs1 + labs1b, loc='upper left')

ax1.set_title('VIX vs 21-Day Realized Vol of SPX')

# Subplot 2: Difference (scaled)

ax2.plot(diff.index, diff,

color='white', linewidth=1,

label='VIX – Scaled Realized Vol')

ax2.axhline(0, color='gray', linestyle='--', linewidth=0.8)

ax2.set_xlabel('Date')

ax2.set_ylabel('Difference')

ax2.legend(loc='upper left')

ax2.set_title('Difference: VIX minus Scaled 21-Day Realized Vol')

# Common X-axis formatting

locator = MonthLocator(bymonth=(1, 4, 7, 10))

formatter = DateFormatter('%Y-%m')

ax2.xaxis.set_major_locator(locator)

ax2.xaxis.set_major_formatter(formatter)

plt.setp(ax2.get_xticklabels(), rotation=45, ha='right')

plt.tight_layout()

plt.show()