When Market Intuition Beats Algorithms

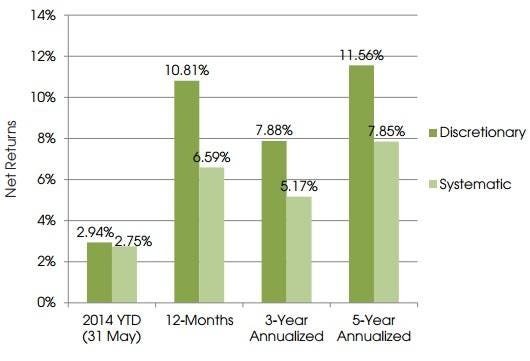

Figure 1. Discretionary hedge funds, i.e. those run by real people making calls, have outperformed systematic, model-driven funds across every major time frame in recent years. Source: IvyPanda.

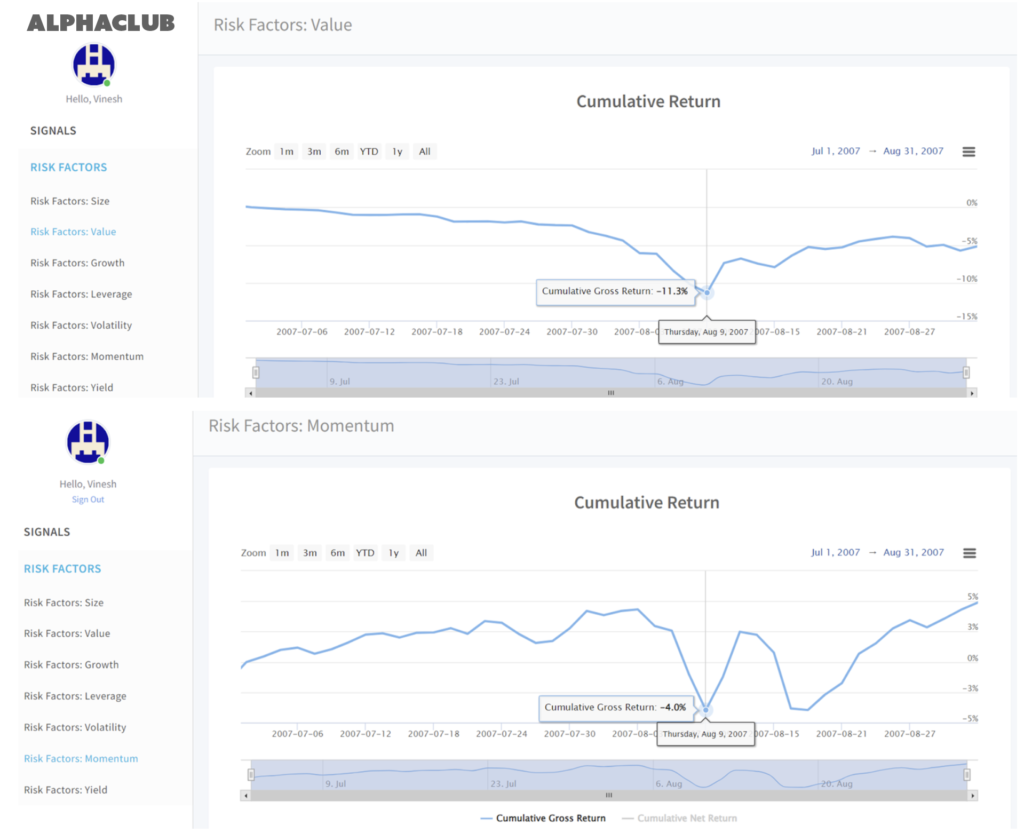

Figure 2. “Quant Quake” in August 2007: Even the best factor models got blindsided. Both value and momentum strategies suffered sudden, sharp drawdowns. Source: ExtractAlpha.

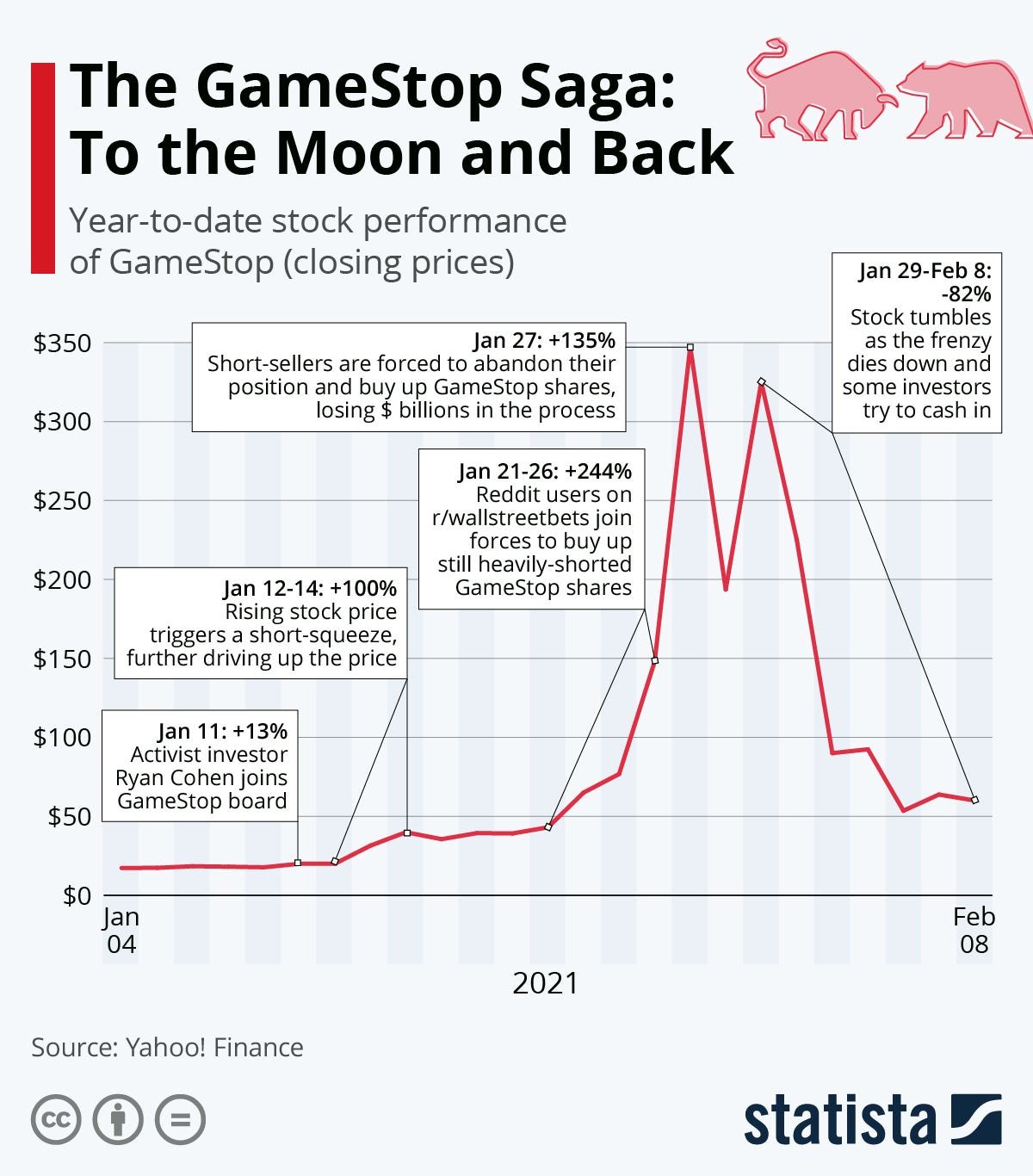

Figure 3. GameStop’s epic 2021 short squeeze: Retail traders fueled a parabolic rally that left most traditional models behind. The price soared over 1,600% in weeks, driven by collective action on social media. Source: Statista, based on Yahoo! Finance data.

Figure 4. This chart shows several years where the S&P 500 kept rising, even as momentum signaled repeated negative divergences. Source: seeitmarket.com.

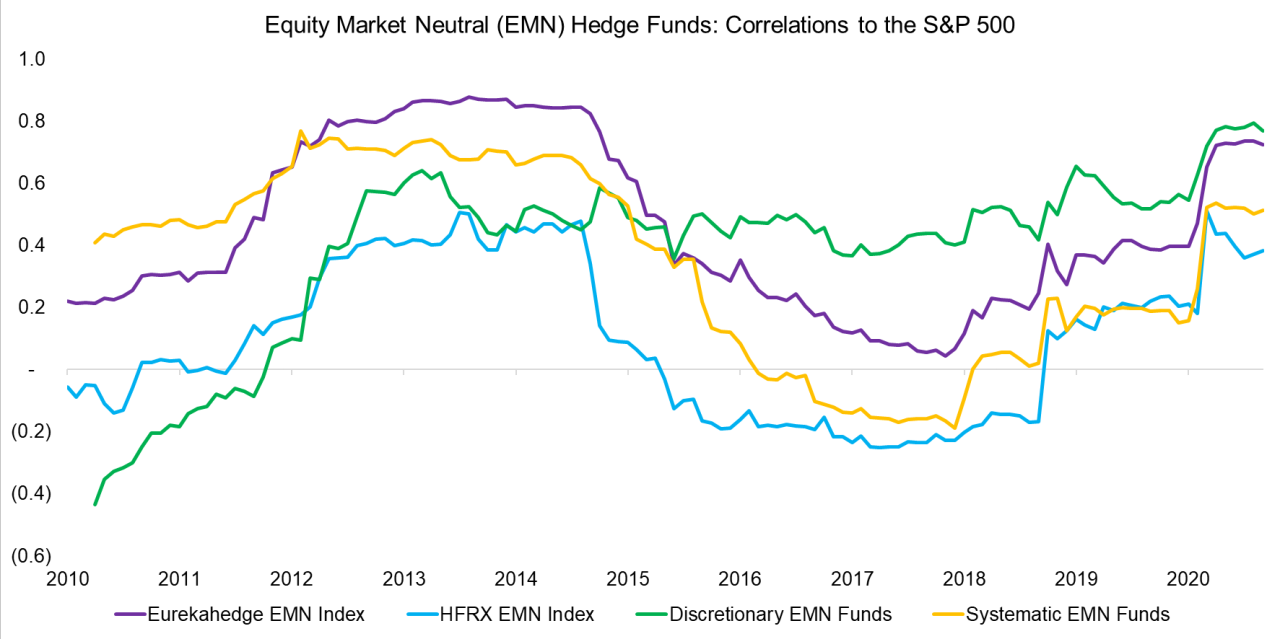

Figure 5. Correlations between equity market neutral hedge funds and the S&P 500. Discretionary and systematic funds show different correlation profiles over time. Source: Karl Rogers via LinkedIn.

Figure 6. 1987 Black Monday crash, where stocks lost nearly 25% in a single session. Source: Investopedia.com.

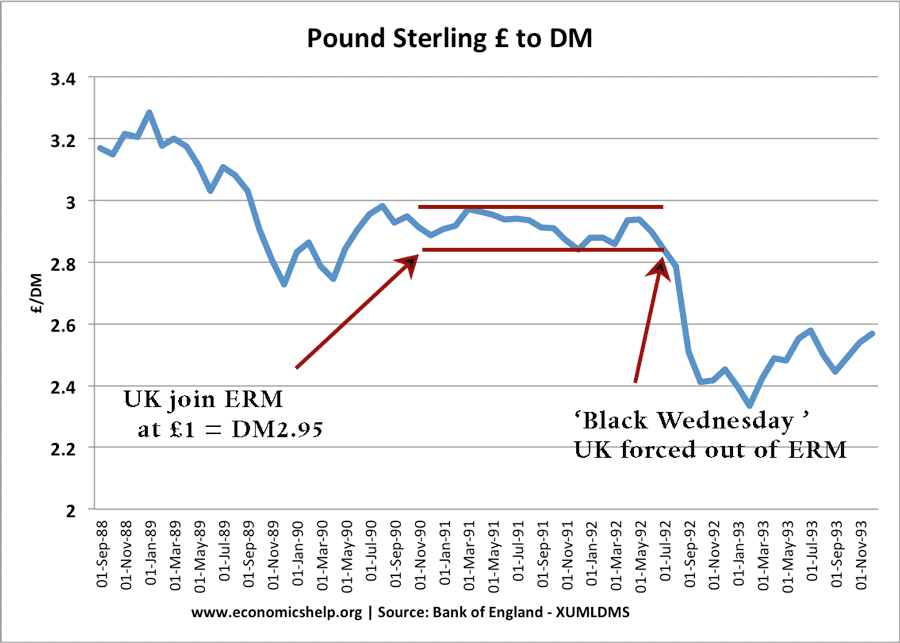

Figure 7. Pound sterling vs. Deutsche Mark, 1988–1993. The chart highlights the collapse of the pound on “Black Wednesday” as the UK exited the ERM, Source: Bank of England / economicshelp.org.

Figure 8. Subprime mortgage originations exploded from 2003 to 2006, with securitized loans reaching record highs and accounting for nearly a quarter of all U.S. mortgages. Source: Inside Mortgage Finance.

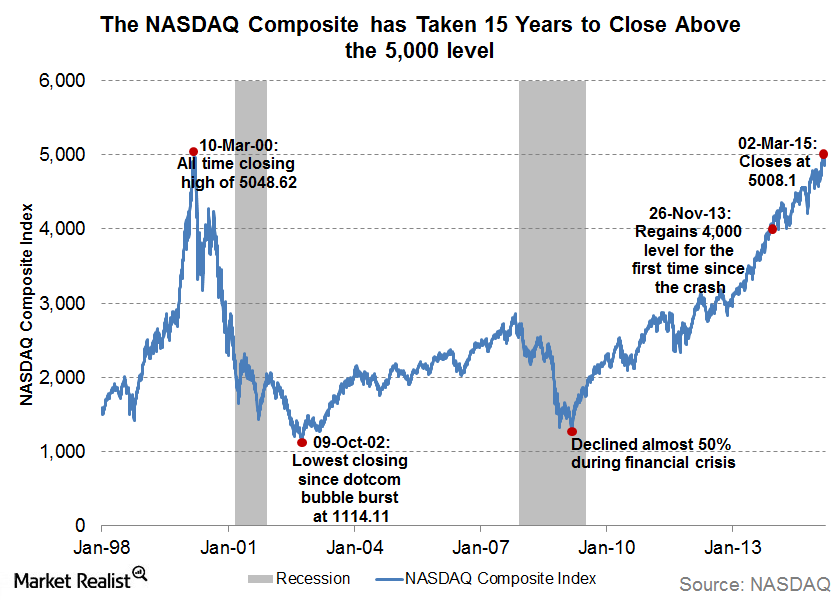

Figure 9. The NASDAQ Composite hit its dot-com bubble peak above 5,000 in March 2000, then collapsed and took 15 years to recover. Source: NASDAQ / Market Realist.

Figure 10. cost of credit default swaps on U.S. investment banks from 2007 to 2020. The spike in 2008 reflects market fears during the subprime crisis, while later surges highlight renewed stress, including during early 2020. Source: IHS Markit / Financial Times.

Newsletter