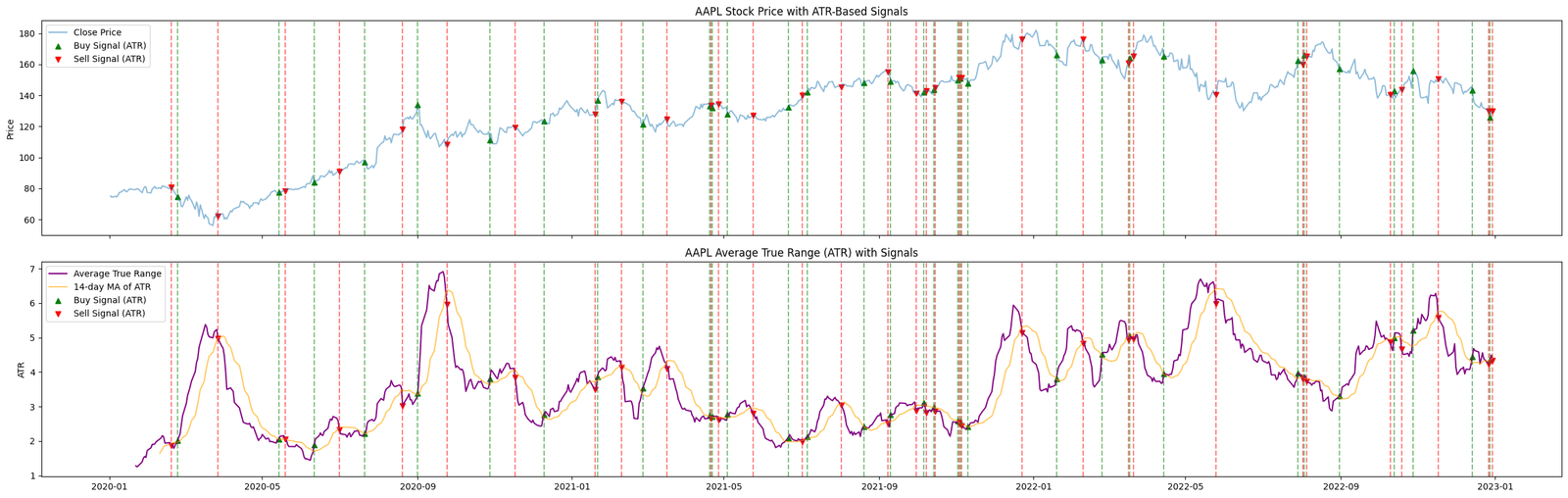

import yfinance as yf

import matplotlib.pyplot as plt

import pandas as pd

# Function to calculate the Average True Range (ATR)

def calculate_atr(data, window=14):

high_low = data['High'] - data['Low']

high_close = abs(data['High'] - data['Close'].shift())

low_close = abs(data['Low'] - data['Close'].shift())

ranges = pd.concat([high_low, high_close, low_close], axis=1)

true_range = ranges.max(axis=1)

atr = true_range.rolling(window=window).mean()

return atr

# Retrieve data

ticker = 'AAPL' # Example ticker

data = yf.download(ticker, start="2020-01-01", end="2023-01-01")

# Calculate ATR and its moving average

data['ATR'] = calculate_atr(data)

data['ATR_MA'] = data['ATR'].rolling(window=14).mean() # 14-day moving average of ATR

# Define buy and sell signals

buy_signal = (data['ATR'] > data['ATR_MA']) & (data['ATR'].shift(1) <= data['ATR_MA'].shift(1))

sell_signal = (data['ATR'] < data['ATR_MA']) & (data['ATR'].shift(1) >= data['ATR_MA'].shift(1))

# Plotting

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(25, 8), sharex=True) # Share x-axis

# Stock price plot with ATR-based buy and sell signals

ax1.plot(data['Close'], label='Close Price', alpha=0.5)

ax1.scatter(data.index[buy_signal], data['Close'][buy_signal], label='Buy Signal (ATR)', marker='^', color='green', alpha=1)

ax1.scatter(data.index[sell_signal], data['Close'][sell_signal], label='Sell Signal (ATR)', marker='v', color='red', alpha=1)

for idx in data.index[buy_signal]:

ax1.axvline(x=idx, color='green', linestyle='--', alpha=0.5)

for idx in data.index[sell_signal]:

ax1.axvline(x=idx, color='red', linestyle='--', alpha=0.5)

ax1.set_title(f'{ticker} Stock Price with ATR-Based Signals')

ax1.set_ylabel('Price')

ax1.legend()

# ATR subplot with buy and sell signals

ax2.plot(data['ATR'], label='Average True Range', color='purple')

ax2.plot(data['ATR_MA'], label='14-day MA of ATR', color='orange', alpha=0.6)

ax2.scatter(data.index[buy_signal], data['ATR'][buy_signal], label='Buy Signal (ATR)', marker='^', color='green')

ax2.scatter(data.index[sell_signal], data['ATR'][sell_signal], label='Sell Signal (ATR)', marker='v', color='red')

for idx in data.index[buy_signal]:

ax2.axvline(x=idx, color='green', linestyle='--', alpha=0.5)

for idx in data.index[sell_signal]:

ax2.axvline(x=idx, color='red', linestyle='--', alpha=0.5)

ax2.set_title(f'{ticker} Average True Range (ATR) with Signals')

ax2.set_ylabel('ATR')

ax2.legend()

plt.tight_layout()

plt.show()