Option-Based Forward Price Forecasting Using Risk-Neutral Probabilities

Forward-Looking Price Probability Estimation

The tool quantifies the likelihood of future stock prices. It converts option prices into a probability distribution that reflects market expectations.

Quantitative Risk and Opportunity Assessment

It evaluates downside risk and upside potential by calculating the probability of price moves across specified ranges and expiration dates.

Account for Minimum Holding Periods

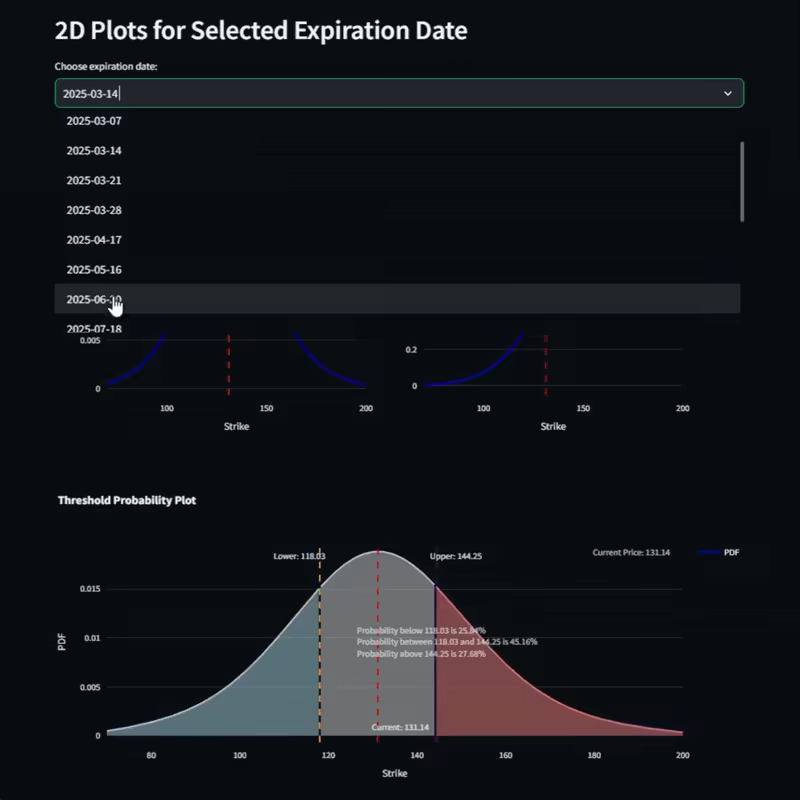

Evaluate the likelihood of price moves within specific thresholds. The tool calculates probabilities below, between, and above key price levels. This supports informed decision making based on market expectations.

Key Features

Computes implied volatility from call option prices using the Black-Scholes model.

Derives a risk-neutral probability density function via the Breeden-Litzenberger formula.

Smooths the probability distribution with Kernel Density Estimation.

Integrates the density function to yield cumulative probabilities for defined price thresholds.

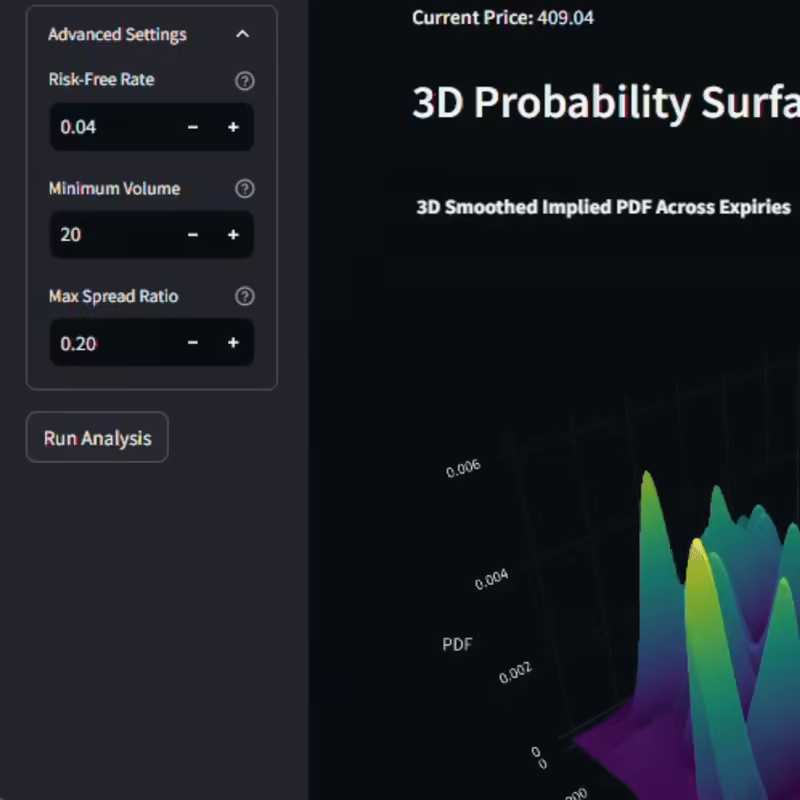

Uses a unified strike grid for consistent analysis across expiration dates.

Real-time data and market expectations on foward looking probabilities