Decomposition of Returns, Factor Exposure and Mispricing Detection

Decompose Portfolio Returns

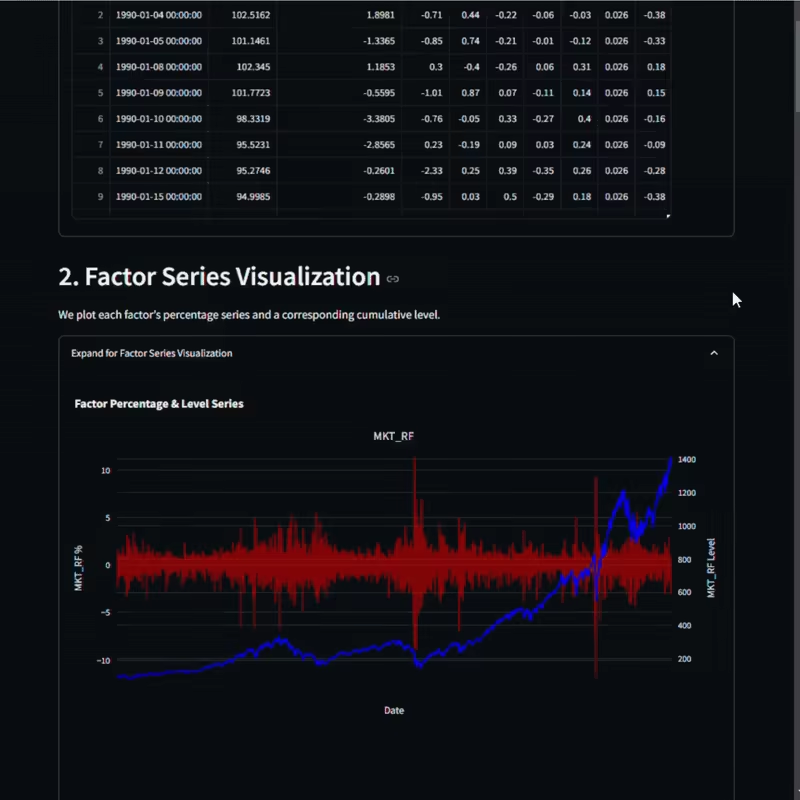

Break down your portfolio’s daily returns into systematic factors and stock-specific effects. Evaluate how market, size, value, profitability, investment, and momentum factors drive returns.

Monitor Factor Exposures Over Time

Track rolling betas and alpha to see how factor sensitivities evolve. Use rolling regressions to detect shifts in risk exposure and potential mispricing.

Valuation and Mean Reversion of Alpha

Assess whether a stock’s excess returns revert to the mean to signal over- or undervaluation and how quickly mispricing corrects.

Key Features

Rolling Regression Analysis: Continuously estimate factor betas and alpha over a user-defined window to reveal dynamic risk exposures.

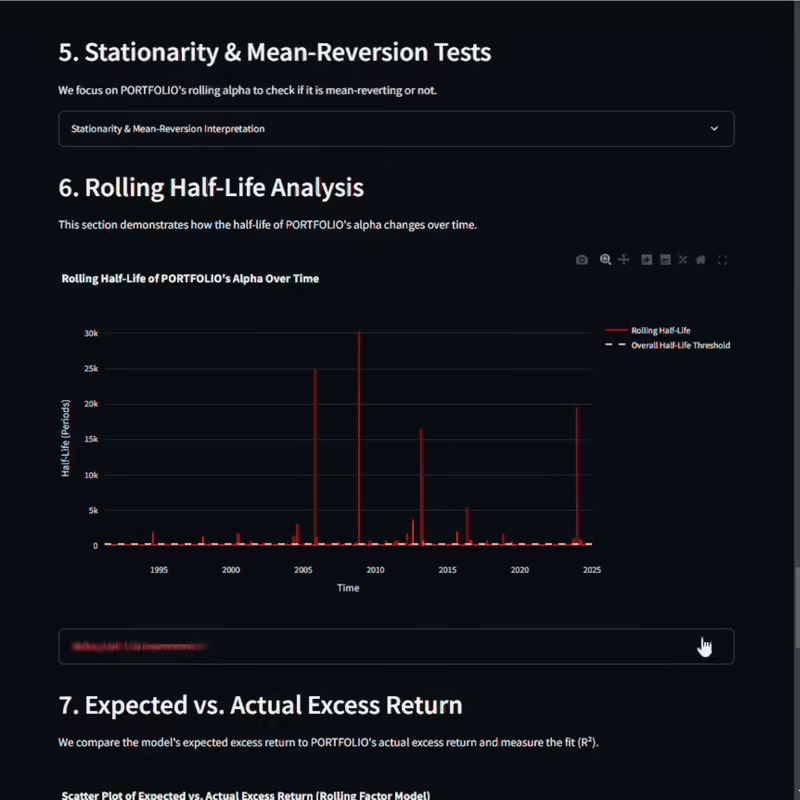

Stationarity & Mean-Reversion Testing: Quantify the persistence of mispricing using rigorous statistical tests.

Half-Life Calculation: Determine how quickly mispricing corrects to guide short- or long-term strategies.

Cumulative Factor Contributions: Visualize and quantify each factor’s impact on excess returns over time.