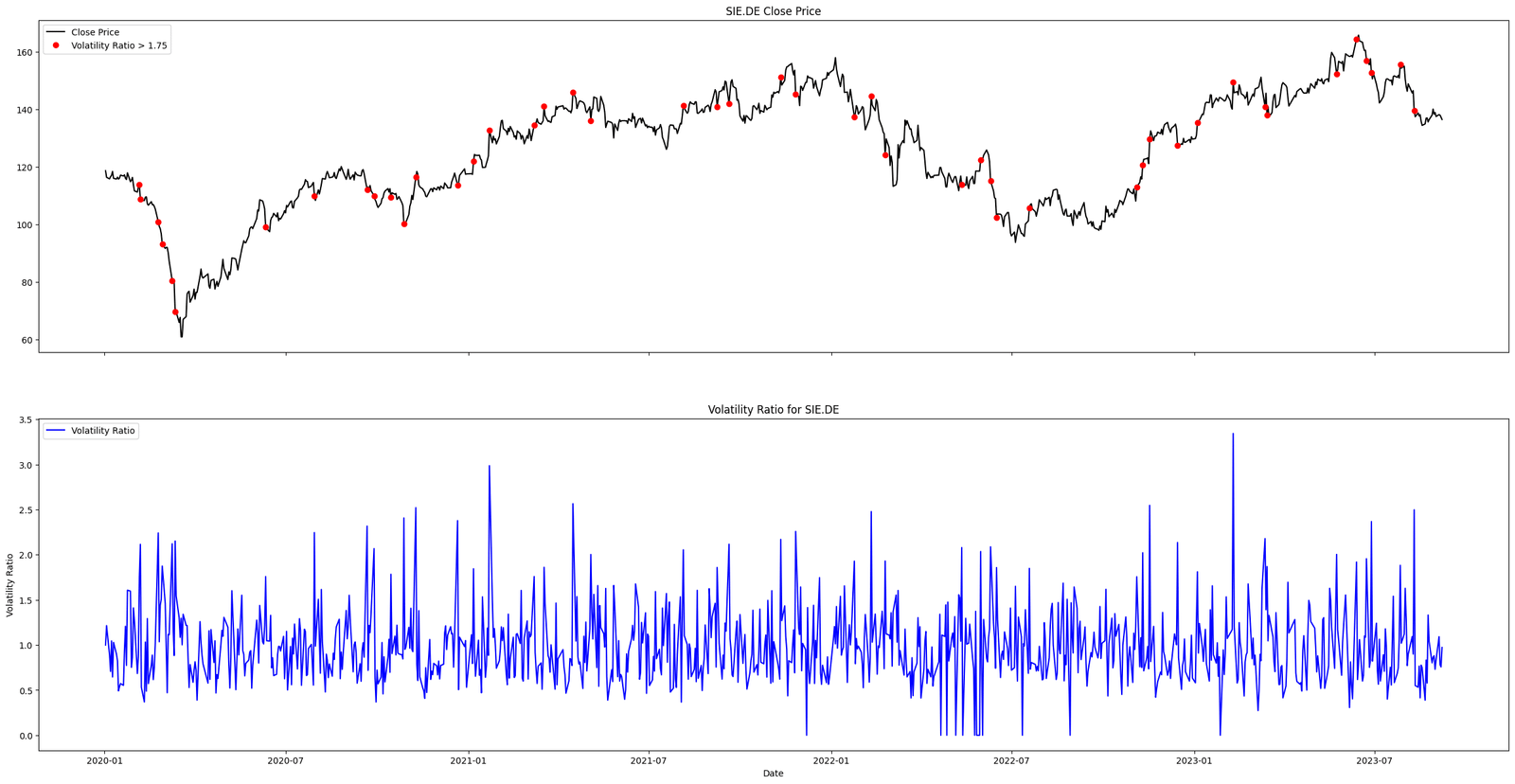

Identify Key Market Shifts with the Volatility Ratio

Figure. 1: This animation illustrates the evolving volatility ratio over a specified time span. As the timeline progresses, observe the fluctuations and zones where the ratio exceeds the defined threshold, giving investors a visual representation of periods of heightened volatility, potential trading interest, and pivotal market moments.

Newsletter

Get Every Weekly Update & Insights

[mc4wp_form id=]