Bootstrapping Future Price Movements Probabilities

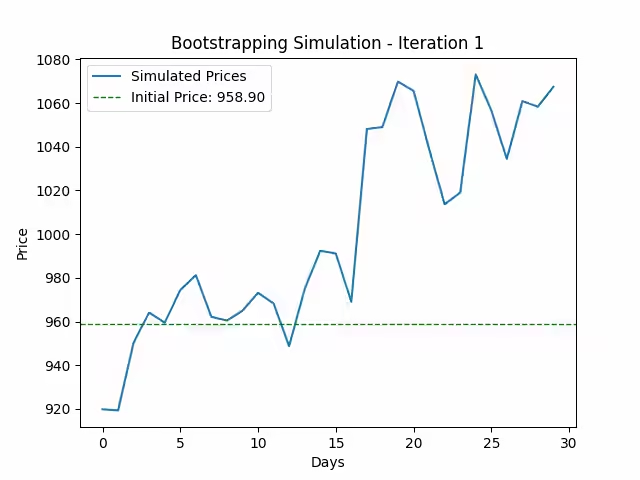

Figure. 1: Bootstrap Simulation: This GIF illustrates the bootstrap simulation process for predicting future stock prices. Each frame shows a new simulated price path generated by resampling historical daily returns with replacement.

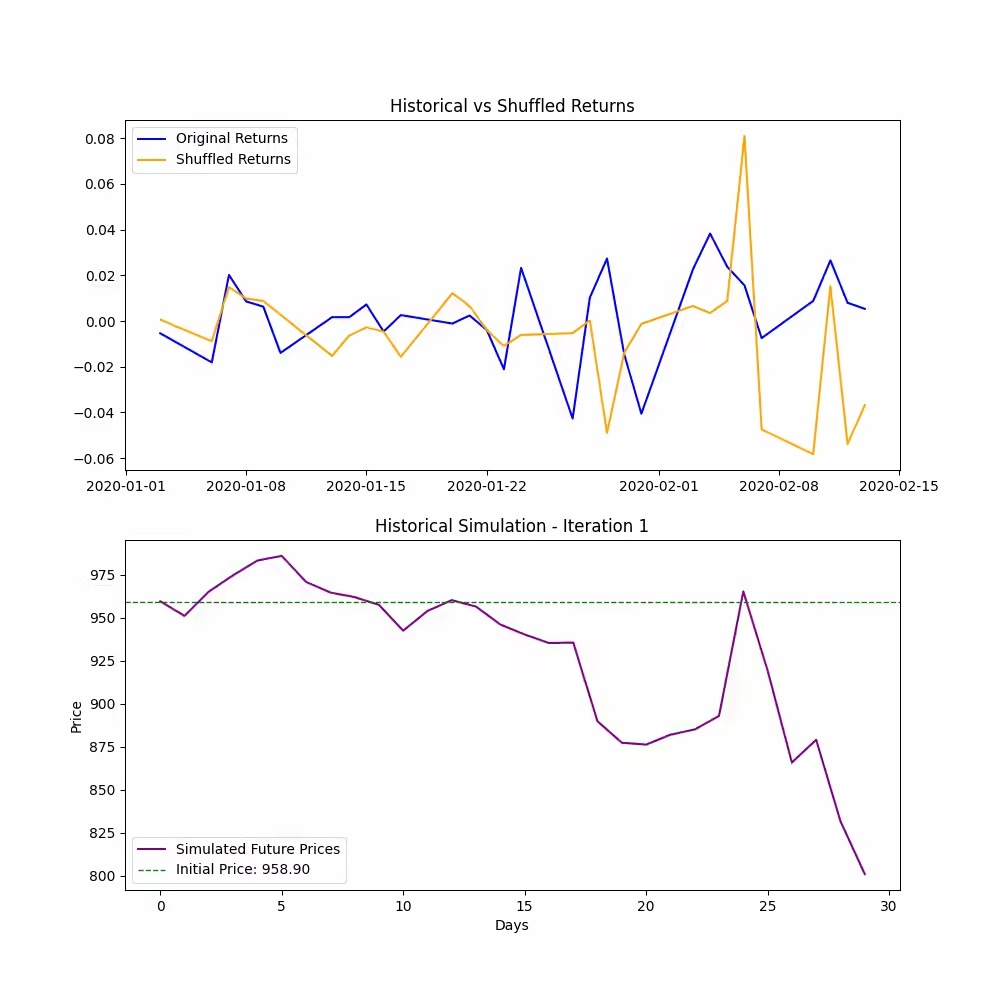

Figure. 2: Historical Simulation: This GIF demonstrates the historical simulation approach for forecasting stock prices. Each frame compares original historical returns to shuffled returns and shows the resulting simulated price path. The process preserves the actual distribution of returns while generating potential future scenarios.

Newsletter

Get Every Weekly Update & Insights

[mc4wp_form id=]