Anchoring VWAP Like Institutions

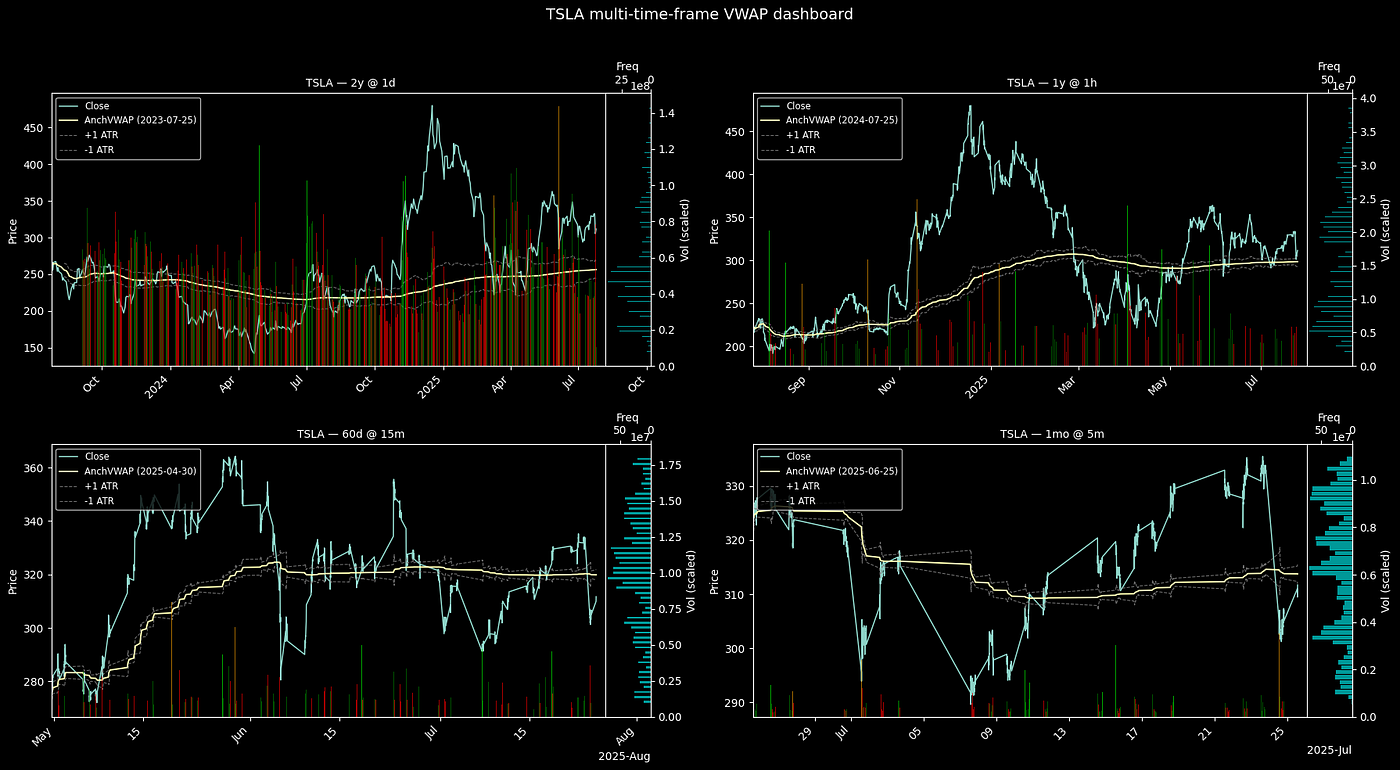

Figure 1. Anchored VWAP (dashed line) acting as a dynamic reference point. Price repeatedly tests this level, with each rejection or breakout signaling a shift in market control. Source: tradebrigade.co.

Newsletter

Get Every Weekly Update & Insights

[mc4wp_form id=]